United Trust Bank (UTB) is a specialist bank based in the UK. Founded in 1955, UTB provides several financial products and services, including bridging loans.

UTB has maintained a positive reputation, particularly in areas like bridging finance, development finance, and structured finance. The bank has won several industry awards over the years, attesting to its expertise and quality of service.

In this review, I will highlight the bank’s main features, detail their fees and rates, and weigh their pros and cons and customer reviews to help you decide if UTB is the right Bridging Finance provider for your needs.

United Trust Bank Bridging

UTB offers a range of regulated and unregulated bridging loans from £125K to £15m for both residential and commercial needs.

These loans can be used to quickly secure the purchase of a property, fund refurbishments, raise capital, or refinance existing loans.

Key features include:

- Regulated and Unregulated Bridging Loans

- Terms up to 12 months (regulated) & 36 months (unregulated)

- 1st, 2nd & Combination Charges

- No Age Limit

- No Early Repayment Charges

- Interest Calculated Daily

- No Mandatory Monthly Repayment

- Legal Representation is Offered

- Automated Valuations are Possible

- Light and Heavy Refurbishment Projects

- Fast Track Process Available

UTB has an overall great reputation and offers 36-month loans, which is relatively rare in the industry. Most of its competitors have a maximum term of 24 months.

UTB’s fast-track option, legal support and competitive rates make it a great option for every borrower profile.

What are the Eligibility Criteria for a UTB Bridging Loan?

Here’s the criteria to apply for a bridging loan with UTB, as well as some related fees.

Regulated Bridging Loan (Standard & Light Refurbishment)

| Criteria | Value |

|---|---|

| Fast-Track Available | ✅ |

| Location | England, Wales & Scotland |

| Loan Size | £125K to £15M |

| Exit Fees | ❎ |

| Daily Interest | After 1 Month |

| Interest Method | Rolled Up Only |

| Completion Fee | 2% on Drawdown |

| Admin Fee | £495 |

| Maximum Loan Term | 12 Months |

Unregulated Bridging Loan (Standard & Light Refurbishment)

| Criteria | Value |

|---|---|

| Fast-Track Available | ✅ |

| Location | England, Wales & Scotland |

| Loan Size | £125K to £15M |

| Exit Fees | ❎ |

| Daily Interest | After 1 Month |

| Interest Method | Rolled Up or Serviced |

| Completion Fee | 2% on Drawdown |

| Admin Fee | £495 |

| Maximum Loan Term | 24 Months |

| Exist Strategy | Realistic but Doesn’t Have to be in Place |

Unregulated Bridging Loan (Heavy Refurbishment)

All Borrowers Criteria

| Criteria | Value |

|---|---|

| Fast-Track Available | ❌ |

| Location | England & Wales / Scotland Considered |

| Loan Size | £200K to £2.5M |

| Exit Fees | ❎ |

| Daily Interest | After 1 Month |

| Completion Fee | 2% on Drawdown |

| Admin Fee | £1.495 |

| Initial Asset Manager Fee | £500 |

| Maximum Loan Term | 24 Months |

| Exit Startegy | Exit Strategy |

Experienced Borrowers Criteria

| Criteria | Value |

|---|---|

| Maximum ILTV | 70% |

| Maximum Works Costs | £1M / 70% of the Initial Value |

| Maximum LTGDV | 70% |

| Maximum Loan Term | 24 Months |

Inexperienced Borrowers Criteria

| Criteria | Value |

|---|---|

| Maximum ILTV | 70% |

| Maximum Works Costs | £500K / 50% of the Initial Value |

| Maximum LTGDV | 70% |

| Maximum Loan Term | 18 Months |

Application Process for UTB Bridging

Applying for a bridging loan with UTB starts with filling out the dedicated application form you can find here.

Once your form is complete, you can send it to UTB’s team, which will be in touch to discuss the next steps with you.

The front-end process is quick and straightforward, with only the application form needed upfront. More due diligence comes before formal approval for larger loans. Overall, UTB looks to deliver efficient bridging finance.

If all goes well, the process can be completed within a few days of the enquiry.

UTB Bridging Loan Rates

Here are the UTB bridging loan rates for 2023. These rates are pretty straightforward and mostly depend on the LTV and the borrower’s experience.

Regulated Bridging Loan Rates (Standard & Light Refurbishment)

| LTV | 1st Charge | 2nd Charge |

|---|---|---|

| < 50% | 0.84% | 0.94% |

| < 60% | 0.89% | 0.99% |

| < 70% | 0.94% | 1.09% |

Unregulated Bridging Loan Rates (Standard & Light Refurbishment)

| LTV | 1st Charge | 2nd Charge | Semi-Commercial |

|---|---|---|---|

| < 50% | 0.84% | 0.94% | From 1.10% |

| < 60% | 0.89% | 0.99% | From 1.10% |

| < 70% | 0.94% | 1.09% | From 1.10% |

Unregulated Bridging Loan Rates (Heavy Refurbishment)

| LTV | Experienced Borrowers | Inexperienced Borrowers |

|---|---|---|

| < 60% | 1.09% | 1.19% |

| < 70% | 1.14% | 1.24% |

UTB Reviews & Ratings

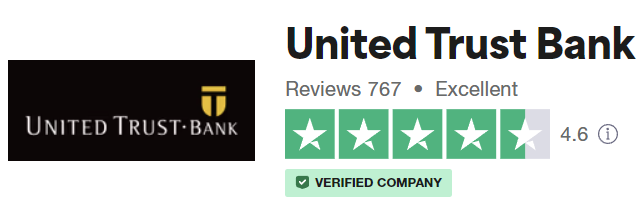

Overall, UTB receives very positive reviews, earning an ‘Excellent’ TrustScore of 4.6 out of 5 based on over 760 reviews on Trustpilot.

The majority of reviews (79%) rate UTB 5 stars. Customers praise the excellent customer service and the competitive interest rates.

12% of reviews are 4 stars. 4% are 3 stars, 1% are 2 stars, and 4% are 1 star. The negative reviews mainly relate to application process delays and difficulties. The bank’s online access is often flagged as fastidious.

However, negative reviews seem limited compared to the general positive feedback. UTB proactively responds to many negative reviews to resolve issues.

In summary, Trustpilot reviews indicate high customer satisfaction with UTB’s lending services, owing to helpful staff and great interest rates for regulated and unregulated bridging loans. While a minority of customers have faced challenges, the overall sentiment toward UTB is very favourable.

Compare bridging loans

Save time and money with Business Expert & Fluent Bridging

Quick Search – Compare bridging loan criteria in real time

Easy Process – Answer a few quick questions about your loan needs

Expert Support – Get access to our partner’s in-house advisers

UTB FAQs

What is the range of loan amounts offered by UTB for bridging loans?

UTB offers bridging loans ranging from £125,000 to £15 million.

What types of properties does UTB accept as security for bridging loans?

UTB accepts residential, HMO (Houses in Multiple Occupation), and mixed-use properties as security. They also consider land with planning and commercial property on a case-by-case basis

What is the Fast-Track process in UTB’s bridging loan service?

UTB’s Fast-Track process is designed for certain applications to expedite the loan approval and disbursement process. The Fast-Track service has a maximum loan size of £500,000, a maximum loan to value (LTV) of 55%, and a maximum of two security properties. The primary exit should be through sale or refinancing.

How quickly can a bridging loan be processed and completed with UTB?

The time taken to complete a bridging loan depends on the specific requirements of the case. However, it can be completed within a few days of the initial enquiry, provided all parties work together effectively, and the valuer has immediate access to the security property if required.

Are there any upfront fees associated with UTB’s bridging loans?

In most cases, the only upfront cost is the valuation fee. However, on limited occasions, UTB may charge an application fee for extremely complicated or time-sensitive cases. Any application fee is refundable upon drawdown of the loan.