Payment gateways are the key link between business sales and the banks that process transactions. If you’re looking to take money from customers online, you can easily integrate one into your website.

You’ll also use a payment gateway if you’re using a card machine or a POS system for in-person transactions. It’s the software that captures the card payment data and relays it to the bank.

In all cases, the best payment gateways make transactions as easy as possible, both for the consumer and the merchant. You’ll need one with low fees, a simple user experience, top-notch security and great customer service.

If you’re short of time:

- Square is an easy, no-contract payment processor to begin with for micro businesses. They charge a transparent 1.4% for online sales. Choose this if you want something very simple or to pair with one of their entry-level card reading machines. Learn more on their website.

- Total Processing is the best payment processor for high-risk businesses with established turnovers (50k+ per month). Visit Total Processing

What is a Payment Gateway?

A payment gateway is a service that facilitates the processing of electronic payments, particularly for e-commerce and online transactions. It acts as an intermediary between a merchant’s website and the financial institutions involved in the transaction.

When a customer makes a payment on a website, the payment gateway securely transmits the payment information to the appropriate financial institution for processing. It ensures that sensitive data like credit card numbers are securely transferred through encryption. The gateway then returns the transaction results to the merchant’s website, enabling the completion of the purchase.

This system is essential for online businesses, as it allows for the secure, efficient, and convenient transfer of funds from the customer to the business.

10 Best Payment Gateways Compared

| Payment Gateway | Stars | Best For | Pros | Cons | Visit |

|---|---|---|---|---|---|

| Square | ⭐⭐⭐⭐⭐ | Large retail businesses | Easy to use. Good for all businesses. Built-in analytics. | Not the cheapest. Lacks multi-currency support. | Square |

| Total Processing | ⭐⭐⭐⭐⭐ | Larger volume, High Risk, API integration | Great customer service, high level of technical capability, price competitive at higher volumes | Not appropriate for smaller businesses. 500k p.a. turnover minimum | Total Processing |

| Stripe | ⭐⭐⭐⭐ | Online businesses, customization | Customizable. Global reach. | Complex for non-technical users. Costly for micro-transactions. | Stripe |

| PayPal | ⭐⭐⭐ | Brand recognition | Trusted brand. Easy setup. | High fees. Account freezing issues reported. | PayPal |

| Worldpay | ⭐⭐⭐⭐ | Global payments, large volume | Global reach. Customizable. Detailed analytics. | Complex features. Tiered pricing can get costly. Long contracts. | Worldpay |

| Adyen | ⭐⭐⭐⭐ | Global enterprises | Multi-currency. Cross-channel consistency. | Complex pricing. Steep learning curve. | Adyen |

| Amazon Pay | ⭐⭐⭐⭐ | Leveraging Amazon’s platform | Increased conversion. Lower cart abandonment. | Limited customization. Dependency on Amazon ecosystem. | Amazon Pay |

| Shopify Payments | ⭐⭐⭐⭐ | Shopify merchants | Unified experience. | Limited to Shopify users. Restricted availability. Currency conversion fees. | Shopify Payments |

| Opayo | ⭐⭐⭐ | Security-focused businesses | Broad payment options. | Complex setup. Not as seamlessly integrated. | Opayo |

| Braintree | ⭐⭐⭐⭐ | Feature-rich solutions | Feature-rich. Seamless experience. | Overkill for small businesses. Accumulating fees. | Braintree |

Square

Square is an all-in-one solution for payment processing. They offer card readers and EPOS machines as well as simple payment gateways you can integrate with all major e-commerce systems.

They’re a good choice for all businesses but the per transaction fee of 1.75% is higher than what you’d get if you entered a longer-term contract with some competitors.

It’s ideal for larger retail businesses such as restaurants, however. Set up a free online store, process payments via social media, or even customise your setup with their free APIs and SDKs.

Connect with Wix, Weebly, Ecwid, BigCommerce, 3dcart, Drupal Commerce, WooCommerce, and Magento with a simple plugin or APP.

Square works with any UK-issued and most international tap, chip and PIN, magnetic stripe cards with a Visa, MasterCard, American Express, Maestro, Visa Electron or Vpay logo.

Pros and Cons of Square

- The user interface is so intuitive that even the most tech-averse can navigate it with ease.

- The hardware variety caters to all—from the countertop register to the pocket-sized mobile card reader.

- The pricing is transparent; you know exactly what you’re going to be charged per transaction, and there are no nasty surprises.

- Analytics and reporting are baked right into the dashboard, allowing businesses to gain actionable insights without needing a separate platform.

- For businesses churning through high transaction volumes, Square will not be the most cost-effective.

- International businesses may find the lack of multi-currency support limiting.

Square Pricing & Fees

Square’s pricing is simple.

For in-person transactions, it’s 1.75% per swipe or tap, and for online transactions, it’s 2.5%. No setup fees, no monthly charges; it’s as straightforward as it gets.

You do pay slightly more for it’s sheer simplicity. Stripe, by comparison, charges 1.5% + 20p for online transactions.

Who Should Use Square?

If you’re a micro business looking for a no-fuss, reliable payment gateway, Square should be on your shortlist. The service is excellent for those who want an all-in-one solution for payments, inventory, and even customer relationship management.

It gets my top vote for best entry level card reader.

Square vs Competitors

While Square is an excellent entry-level choice for its user-friendly interface and no monthly fees, it becomes less cost-effective as transaction volumes increase. In comparison, Stripe, Worldpay, and Total Processing offer more competitive pricing structures at higher volumes.

Stripe, in particular, is renowned for its API flexibility and developer-friendly platform, making it a preferred choice for businesses requiring custom payment solutions. Worldpay offers a wide range of payment processing options and is known for its robust security features, making it suitable for larger, more established businesses.

Total Processing distinguishes itself by catering to a diverse range of niches, offering bespoke solutions tailored to specific industry needs. This flexibility makes it an attractive option for businesses with unique requirements or those operating in specialised markets.

Total Processing

Total Processing is a Manchester-based fintech company (bought by NomuPay in 2023), known for offering a very broad and technically competent range of payment processing services. They are the ideal choice for those who operate in higher-risk sectors, such as dropshipping, CBD, adult, gambling or crypto.

They are distinguished by their flexible pricing, diverse services, and very strong emphasis on customer service. They can get you set up extremely fast and, while they don’t produce hardware themselves, can easily get you integrated with any type of EPOS system. They accept over 190 payment methods, which is more than any other provider we’ve analysed.

Pros and Cons of TotalProcessing

- Competitive Pricing: If your volume of sales is enough, Total Processing claim their rates are unbeatable

- Complex Integration Options: Offers easy integration with popular platforms, facilitating seamless payment processes.

- Diverse Services: Provides a variety of services including POS systems, online payment processing, and fraud prevention, suitable for both digital and physical outlets.

- No Flat Rate Pricing: Pricing varies depending on business needs, which may be a challenge for small businesses seeking predictable costs.

Pricing

Total Processing offers competitive fees and charges, with both interchange-plus and tiered pricing models. Businesses receive custom quotes based on their transaction volume, industry, and risk assessment, ensuring pricing is tailored to specific needs. They can provide month-to-month contracts with no long-term commitment or longer term contracts for better rates.

Who Should Use Total Processing

Total Processing is suitable for medium-sized businesses (SMBs) turning over at least 40k monthly. They also serve a wider variety of high-risk sectors than any other provider on the market.

Choose them if you need:

- Customised Payment Solutions: Tailored services for unique business needs, including high-risk merchant accounts.

- Flexible Pricing Options: Ideal for businesses seeking competitive and negotiable rates.

- Extensive Payment Method Support: Businesses looking to accept a wide range of payment methods, including 198+ alternative payment methods globally.

- Strong Customer Support: Access to dedicated support teams available 24/7, beneficial for businesses requiring constant assistance.

- High-Risk Sector Support: A good fit for sectors like online gambling, CBD, e-cigarettes, adult industries, and others requiring specialised payment processing solutions.

Total Processing vs Competitors

In contrast to Stripe, which is celebrated for its API flexibility and developer-oriented features, Total Processing offers a similarly high level of API adaptability but with a stronger focus on bespoke solutions. This focus makes it an excellent option for businesses that require highly customised payment processing services.

Comparing Total Processing with other high-risk sector competitors like Verotel, Epoch Payment Solutions, and Instabill, Total Processing stands out for its significantly broader range of payment methods, supporting over 198+ options globally. This extensive reach, coupled with its ability to customise services for high-risk industries, gives it a competitive edge.

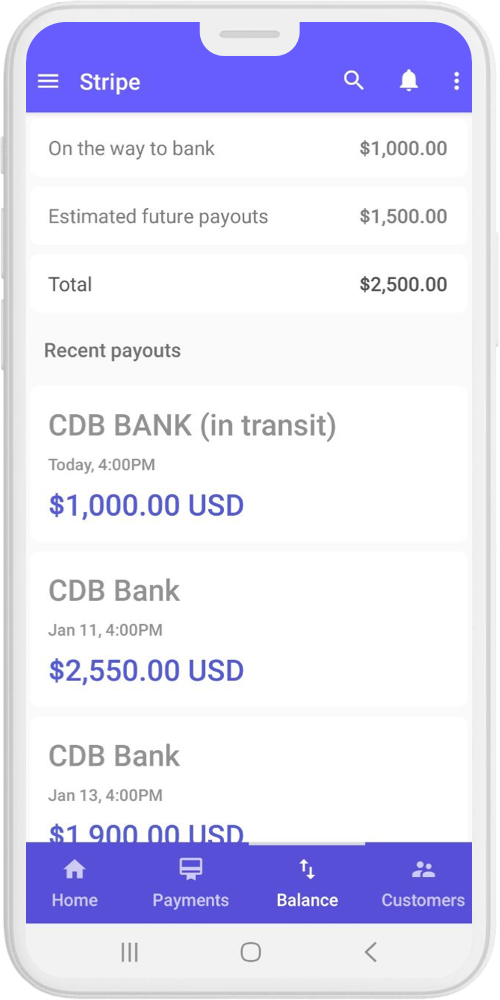

Stripe

Stripe is an excellent choice for businesses requiring a multi-functional platform capable of handling subscriptions, invoices, and fraud protection. Stripe’s support for multiple currencies and payment methods is a significant advantage for those looking to expand globally.

However, the platform’s extensive range of features can also be a drawback, particularly for smaller businesses that may find themselves paying for functionalities they don’t necessarily need. Stripe’s pricing model, while transparent, can become costly as you add more advanced features or if you process large volumes of transactions.

Another point of consideration is the technical expertise required to maximise Stripe’s full potential. While it offers pre-built solutions for those without a technical background, businesses looking to customise extensively may need a skilled developer. This could add an additional layer of cost and complexity.

Lastly, while Stripe offers various pre-built integrations, your current software stack may not be fully compatible, necessitating additional time and resources for custom integration.

Pros and Cons of Stripe

- Extensive API Accept payments in over 135 currencies.

- High Scalability

- Can handle massive volume

- May not be suitable for non-technical users.

- Costly for Micro-Transactions

- Up to seven-day settlement delay

- If a customer uses a card in a currency different from your checkout’s usual one, there’s an extra 2% fee added to the basic transaction fee.

- Difficult to speak with a human support representative

Stripe Pricing & Fees

Stripe offers a pay-as-you-go pricing model. Domestic transactions are charged at 1.5% + 20p for European cards and 2.5% + 20p for non-European cards. There are no setup or monthly fees.

Using a payment link is more cost-effective at 1.2% + 20p for all UK cards.

Additional services like subscriptions or international payments come with their own pricing.

Who Should Use Stripe?

Stripe is well-suited for online businesses that require a flexible, scalable payment solution. It’s particularly beneficial for companies with a global reach due to its multi-currency support. Moreover, its rich API environment makes it an excellent choice for those comfortable with custom coding.

Stripe vs Competitors

Stripe’s key competitors include Adyen, Shopify, Square, PayPal, and Total Processing, each offering unique features and strengths.

Adyen is known for its broad global payment infrastructure, appealing to large, international businesses needing a wide range of currency and payment method options. Its comprehensive approach to payment processing makes it ideal for businesses looking to consolidate their payment systems under one provider.

Shopify, primarily an e-commerce platform, offers integrated payment solutions through Shopify Payments. This integration is particularly advantageous for e-commerce businesses using Shopify’s platform, providing a seamless payment experience for both the business and its customers.

Square, similar to Stripe, is user-friendly and ideal for small businesses and startups. However, as transaction volumes increase, Square’s cost-effectiveness decreases compared to Stripe’s more scalable pricing structure. Square’s simplicity in setup and use makes it a great entry-level option for new businesses.

PayPal is a household name, recognised for its wide consumer base and ease of use. While it offers flexibility and a high level of consumer trust, its fee structure can be higher compared to Stripe, especially for international transactions.

Total Processing differentiates itself by focusing on bespoke solutions, particularly for high-risk sectors and businesses with unique processing requirements. While Stripe offers extensive API customisation, Total Processing provides tailored services that address specific industry needs, making it a viable choice for businesses in specialised markets.

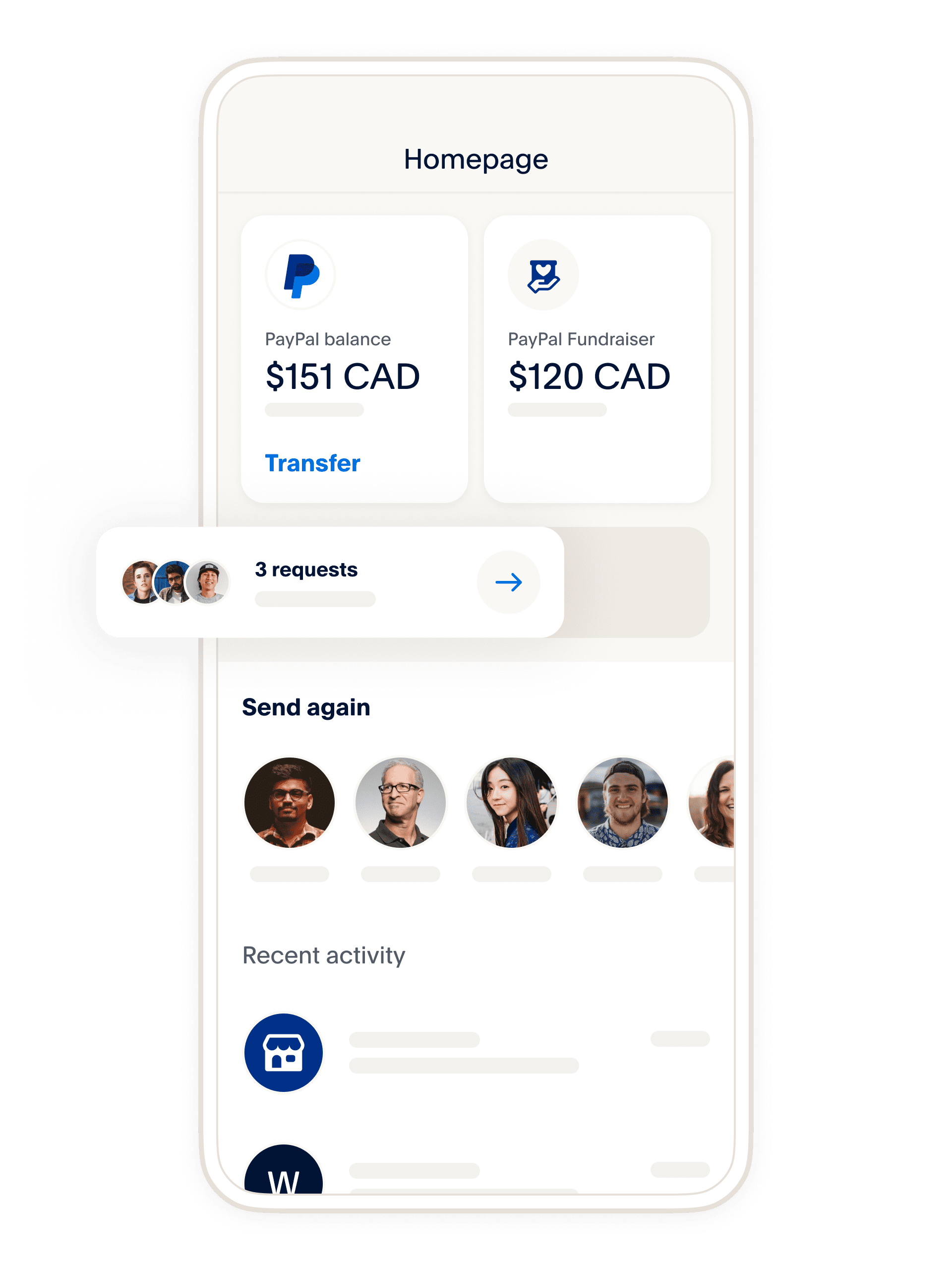

Paypal

PayPal is one of the most widely recognized and used payment gateways in the world and a very reliable way to take payments. PayPal’s broad adoption offers instant credibility for merchants, along with a range of features from invoice creation to subscription billing.

I wouldn’t suggest you use PayPal as your only payment gateway simply because the fees are amongst the highest. But it’s useful as a secondary integration because it’s so commonplace. It also supports over 200 currencies and accepts payments from over 200 countries.

Pros & Cons

- Consumer Trust: PayPal is well-known and widely trusted, potentially increasing conversion rates.

- Versatility: Suits businesses of all sizes and types, with various options for payment acceptance.

- Easy Setup: Intuitive and straightforward, requiring minimal technical skills.

- Higher Transaction Fees: Generally, PayPal’s fees are on the higher side compared to competitors.

- Account Freezing: There have been reports of sudden account limitations or freezes, affecting cash flow.

PayPal Pricing & Fees

PayPal levies a fee of 2.9% plus £0.30 per transaction for domestic sales within the UK. For international transactions, the rate climbs to 4.4% per transaction, in addition to a fixed fee that varies depending on the currency involved.

While there are no initial setup or ongoing monthly fees, additional charges may be incurred for services such as chargebacks.

Who Should Use PayPal?

Given its ubiquity and ease of use, PayPal is suitable for both any type of business. It’s particularly useful for those who wish to reach a broad, international customer base, given PayPal’s widespread recognition and trustworthiness.

PayPal vs. Competitors

In contrast to Stripe’s focus on customizability and API options, PayPal offers a ready-to-use solution that appeals to businesses seeking to get started quickly. However, its fee structure makes it potentially more expensive for micro-transactions.

- Square stands out for its appeal to small businesses and brick-and-mortar stores with its integrated POS systems and straightforward fee structure. While PayPal offers broader online payment solutions, Square excels in providing a comprehensive in-person payment system, making it a preferred choice for retail businesses.

- Adyen offers a robust, global payment infrastructure that serves well for large-scale, international businesses. Adyen’s strength lies in its ability to handle a variety of currencies and payment methods, making it suitable for businesses with a global presence, in contrast to PayPal’s more general, consumer-focused approach.

- Shopify Payments, integrated within Shopify’s e-commerce platform, is particularly advantageous for online retailers using Shopify. Its seamless integration for online sales makes it a more convenient choice for these businesses compared to PayPal, which, while versatile, requires separate integration with e-commerce platforms.

- Total Processing differentiates itself with bespoke solutions, especially for businesses in high-risk sectors or those requiring specialised payment processing services. This focus on tailored solutions offers an alternative to PayPal’s more standardized offerings.

Worldpay

Worldpay is a comprehensive global payment gateway, serving over 146 countries and offering more than 300 payment methods. Apparently they process some 26 million transactions a day, and they are certainlyt one of myt top providers.

They’re secure, great for multi-currency support, and can help your business offer card payments, online payments, mail and phone payments with ease. Choose from pay-as-you-go or pay monthly, and you’ll also get excellent customer servive which receives consistently good reviews.

The pay as you go rates aren’t the cheapest (2.75% of each transaction plus a fixed fee of £0.20) but it gets more competitive once you go onto a contract. That said, their contracts are quite long: typically a standard three-year contract with an auto-renewal clause that means you’ll be signed up for an additional year at the end.

Pros & Cons

- Global Reach: Extensive support for international transactions, including a plethora of currencies and payment methods.

- Security Measures: Advanced fraud protection and secure data encryption.

- Comprehensive Reporting: Provides detailed analytics and transaction reports for deeper business insights.

- Complexity: The platform’s extensive features can be overwhelming for small businesses.

- Fees: Costs can accumulate through a tiered pricing structure and additional service fees.

Worldpay Pricing & Fees

Worldpay has a complex pricing model that can be customized based on your specific business needs. Typically, businesses will encounter a setup fee, monthly fees, and variable transaction charges depending on the payment methods used. Exact details require consultation with Worldpay.

Who Should Use Worldpay?

Worldpay is the right choice if you’re happy to enter into a contract for at least three years. It’s a huge and reliable company used by over 250,000 UK SMEs, and probably the best for integrations. Be warned that if you leave the contract early, they will still charge you the full amount.

Worldpay vs Competitors

- Stripe’s strength lies in its ease of integration with various systems and applications, making it a preferred choice for tech-savvy businesses, a contrast to Worldpay’s more traditional and diverse payment processing options.

- Opayo (formerly Sage Pay) While Worldpay provides a wider range of services globally, Opayo is often preferred by UK-based businesses for its localized services and strong customer support.

- Shopify offers an integrated payment solution, Shopify Payments, which is seamlessly integrated with its e-commerce platform. This is particularly advantageous for online retailers using Shopify’s system. Worldpay, in contrast, offers more flexible solutions that can cater to a broader range of businesses, not limited to e-commerce.

- Clover provides an all-in-one POS and payment system, which is particularly beneficial for retail and restaurant businesses. While Clover offers a more hardware-focused solution, Worldpay provides a wider range of payment processing services, including online, mobile, and in-person payments.

- Adyen is a global payment company offering a wide range of currency and payment method options, catering to large international businesses. Adyen’s global reach and ability to handle complex payment structures make it a strong competitor to Worldpay, especially for businesses looking to expand internationally.

Adyen

Adyen is a huge global payment company based in the Netherlands. Often considered a competitor to Stripe, is one of Europe’s largest fintech with a market capitalization of approximately 23.4 billion. They’re an all-in-one payments processor that delivers payments over online, mobile and in-store channels.

Adyen is a good solution for a large firm because it has a larger global network of banks and acquirers than Stripe or Worldpay. It also has very sophisticated risk management system and a scalable infrastructure. They handle high volumes of transactions for some of the world’s largest companies, such as Spotify, Uber, and Airbnb.

Pros & Cons

- Multi-Currency Support: Adyen offers the ability to accept payments in over 150 currencies.

- Cross-Channel Consistency: Provides a unified payment experience across online, mobile, and in-store environments.

- Advanced Analytics: Offers real-time reporting features that provide deep insights into payment performance.

- Steeper Learning Curve: Given its robust set of features, it may take time for businesses to fully exploit its capabilities.

Adyen Pricing & Fees

Adyen employs a blended pricing model that includes a processing fee and a payment method fee. The exact cost can vary depending on the payment methods used, transaction volume, and other factors. Overall they are competitive but not suited to micro businesses.

Who Should Use Adyen?

Adyen is a great fit for mid-to-large enterprises that require a multi-currency, multi-payment method solution, particularly those that operate in multiple markets. Its advanced analytics features also make it suitable for businesses focused on data-driven decision-making.

Adyen vs Competitors

- PayPal is highly recognized for its consumer trust and ease of use, especially in online transactions. It’s a popular choice for small to medium-sized businesses and individual users. Adyen, in contrast, offers more extensive global payment options, appealing to larger businesses with international transactions.

- Worldpay provides a broad range of payment processing services across various channels, making it a versatile option for businesses of all sizes. While Worldpay offers more traditional payment solutions, Adyen excels in handling complex, multi-currency transactions, making it ideal for businesses with a global presence.

- Square is particularly appealing to small businesses and brick-and-mortar stores with its integrated POS systems and user-friendly interface. Adyen, offering a more comprehensive set of global payment solutions, is better suited for larger businesses or those with a significant online presence.

- Braintree, a division of PayPal, is known for its strong focus on online and mobile payment solutions with robust development tools. While Braintree provides a more specialized set of services, particularly in mobile payments, Adyen offers a broader range of payment options and currencies, catering to a wider international market.

- Total Processing distinguishes itself by offering bespoke solutions, especially for businesses in high-risk sectors or those requiring specialized payment processing services. Adyen, offering a global reach with a wide variety of payment methods, appeals more to businesses looking for extensive international transaction capabilities.

Amazon Pay

Amazon Pay stands out as a good choice for boosting conversion rates on your e-commerce site. With such a huge proportion of online shoppers already having Amazon accounts with saved payment details, they can checkout process faster and easier, reducing cart abandonment.

The familiar Amazon branding also adds a layer of trust, encouraging more customers to complete their purchases. Overall, its streamlined and trusted platform can significantly help in converting browsing into actual sales.

It’s worth pointing out Amazon Pay is focused on online payment solutions and doesn’t offer any card readers or Electronic Point of Sale (EPOS) systems. It’s designed to integrate with your online storefront to facilitate smooth transactions, rather than handling in-person sales.

Despite all this, Amazon charges a payment processing fee of 2.7 per cent and an authorisation fee of 30p per transaction, if your monthly payment volume is under £50,000. This makes is significantly more expensive than many competitors and therefore not something we recommend.

- Seamless integration into the Amazon ecosystem, beneficial for businesses targeting Amazon’s large and loyal customer base.

- Lower cart abandonment rates owing to streamlined checkout processes.

- High-level security features, backed by Amazon’s robust fraud protection.

- Quite expensive

- Limited customisation options compared to other gateways.

- Heavy dependency on the Amazon ecosystem could be a drawback for some.

Amazon Pay Pricing & Fees

- Transaction fees vary based on the country but generally range from 2.7% + £0.30 per transaction.

- No monthly fees or setup costs.

Who Should Use Amazon Pay

This payment gateway is particularly beneficial for established online businesses that want to leverage Amazon’s extensive user base and are looking for a highly secure, trusted payment solution.

Amazon Pay vs Competitors

Amazon Pay vs PayPal: – Compared to PayPal, Amazon Pay has a more niche appeal. PayPal’s widespread recognition and trust transcend the e-commerce sector, extending to various types of online transactions and services. While Amazon Pay benefits from the ease of use for existing Amazon customers, PayPal’s independent platform serves a broader audience and is often preferred for its universal applicability and strong brand presence outside the Amazon ecosystem.

Amazon Pay vs Stripe: When comparing Amazon Pay to Stripe, the key distinction lies in their target audience and customization capabilities. Amazon Pay’s strength is in its direct integration with Amazon’s services, offering a straightforward and familiar payment process for Amazon users. In contrast, Stripe is renowned for its API flexibility and the ability to offer highly customizable payment solutions. Stripe caters to businesses looking for bespoke payment systems, particularly those with a strong online presence or technical requirements.

Shopify Payments

Shopify Payments is the native payment gateway for the Shopify e-commerce platform. Engineered for seamless integration with Shopify stores, it streamlines the payment process, making it simpler for business owners to manage transactions within the Shopify interface.

Pros & Cons

- Full integration with Shopify makes for a unified administrative experience.

- Competitive transaction fees when operating within the Shopify ecosystem.

- Advanced fraud analysis tools are included.

- Restricted availability in certain countries and for some types of business.

Shopify Payments Pricing & Fees

- Standard Shopify charges apply, starting at 2.9% + 30¢ per transaction for the basic plan.

- Additional fees for international transactions and currency conversions.

Who Should Use Shopify Payments

Businesses that are already using or planning to use Shopify for their online store will find Shopify Payments to be an extremely convenient solution, designed to function seamlessly within the Shopify platform.

Opayo

Opayo, formerly known as Sage Pay, is a payment service provider based in the UK that offers a range of payment solutions, including online card processing, phone payments, and invoice payments. It’s known for its strong security features and compliance with high-level encryption and anti-fraud protocols.

Pros & Cons

- Offers a broad range of payment options, from online and mobile to over-the-phone transactions.

- Strong security measures, including PCI DSS compliance and robust fraud prevention tools.

- No hidden fees; pricing structure is transparent and straightforward.

- Initial setup can be complex and may require some technical skills.

- Not as seamlessly integrated into all e-commerce platforms compared to other providers.

- Charges for some additional services can accumulate.

Opayo Pricing & Fees

- A flat monthly fee starting from £19.90 per month for up to 350 transactions.

- Custom pricing available for larger businesses requiring a greater volume of transactions.

Who Should Use Opayo

Opayo is best suited for UK-based SMEs that require a variety of payment options and prioritize security. It’s also a good fit for businesses that prefer a flat monthly fee to a per-transaction cost.

Braintree

Braintree is a full-stack payment platform known for its ease of use and seamless integration capabilities. Owned by PayPal, it provides a range of features such as mobile payments, subscription billing, and foreign currency acceptance. The platform is designed to make complex payment needs simple, allowing businesses to focus more on their operations and less on payment processing.

Pros & Cons

- Robust suite of features, including mobile payments, recurring billing, and multiple currency options.

- Seamless integration with a variety of e-commerce platforms and shopping carts.

- Strong security protocols including fraud detection and PCI compliance.

- Given its feature-rich nature, it might be overkill for smaller businesses.

- Transaction fees can accumulate and become significant for businesses with high volume.

- Could pose challenges for businesses that require highly customized solutions.

Braintree Pricing & Fees

- 1.9% + £0.20 per transaction for European cards.

- 2.9% + £0.20 per transaction for non-European cards.

- Additional fees for add-on services like advanced fraud protection.

Who Should Use Braintree

Braintree is suitable for businesses that require a multifaceted payment solution capable of handling various payment types and currencies. Its seamless integration makes it a good choice for those who need to scale quickly.

How Payment Gateways Work

At its core, a payment gateway functions as a digital intermediary, facilitating the exchange of financial information between the different parties involved in a transaction.

When a customer initiates a payment, the payment gateway securely captures and encrypts the payment details and routes them to the merchant’s acquiring bank. The acquiring bank then forwards the information to the issuing bank for verification.

The payment gateway waits for the issuing bank’s response, which confirms whether the transaction is approved or declined. Upon receiving this feedback, the payment gateway conveys the status back to the merchant’s system, allowing the transaction to proceed to completion or be halted.

From a business standpoint, the reliability and efficiency of this process are crucial. A delay or failure in the payment gateway chain can lead to abandoned carts, lost sales, and diminished customer trust. Furthermore, a gateway’s ability to handle multiple payment methods and currencies becomes particularly relevant for businesses with a diverse or international customer base.

How to Choose the Best Payment Gateway

Choosing a payment gateway is a critical decision for businesses of all sizes. It can have a lasting impact on your operations, customer experience, and bottom line.

When evaluating potential options, it’s important to go beyond mere functionality and consider a range of criteria, including:

- Fees and pricing structure: Compare the upfront setup fees, transaction fees, monthly subscriptions, and any potential hidden charges to ensure that the total cost of ownership aligns with your budget.

- Integrations and compatibility: Consider the gateway’s ability to integrate seamlessly with your existing technology stack, including your e-commerce platform, point-of-sale system, and accounting software.

- Reporting and analytics: Sophisticated reporting tools can offer valuable insights into customer behavior, sales trends, and transaction success rates. This data can be used to inform strategic decision-making and performance optimisation.

- Security and compliance: Since payment gateways handle sensitive financial information, robust security features and compliance with industry standards like PCI DSS are essential.

- Scalability and flexibility: Choose a gateway that can scale in line with your growth plans, whether that entails expanding to new markets or adding additional payment methods.

- Customer support: Consider the support channels available and their responsiveness to ensure that you can get assistance when you need it most.

Setting Up a Payment Gateway

The basic steps to integrate a payment gateway with your website or POS system are generally as follows:

1. Research and Compare: Start by exploring different payment gateways. Look for ones that offer competitive fees, reliable customer support, and the features that best fit your business needs.

2. Check Compatibility: It’s crucial to choose a payment gateway that integrates seamlessly with your website or Point of Sale (POS) system.

3. Account Registration: Sign up with your chosen gateway. You’ll need to provide some business details and documentation as part of the process.

4. Customise Settings: Adjust the gateway settings according to your business requirements, such as selecting the currencies you accept, setting up tax calculations, and choosing which payment methods to offer.

5. Implement the Gateway: Integrate the payment gateway into your website or system. Depending on your setup, this could involve some coding or simply adding a plugin or application.

6. Secure Your Site: Install an SSL certificate on your website to ensure all transactions are secure and customer data is protected.

7. Conduct Test Transactions: Before going live, run test transactions to verify that the payment process works smoothly.

8. Legal Compliance: Ensure your business adheres to necessary legal requirements, like the Payment Card Industry Data Security Standard (PCI DSS) for handling card payments.

9. Establish a Refund Policy: Clearly define and display your refund and return policies to your customers.

10. Launch: After thorough testing and ensuring compliance, activate the payment gateway for customer transactions.

What types of businesses are payment gateways suitable for?

Payment gateways are versatile and can be used by a wide range of businesses, including:

- Online retailers: E-commerce platforms need a secure and efficient way to handle online payments.

- Brick-and-mortar stores: Physical retail outlets can benefit from integrated payment gateways in their POS systems for more payment options and faster checkout.

- Subscription services: Businesses that offer subscription-based products or services can automate recurring charges through payment gateways.

- Digital services: Companies that sell digital products, software, or online courses can utilize payment gateways for instant access post-purchase.

- Nonprofits: Charitable organizations can use payment gateways to securely process donations online.

- B2B companies: Business-to-business operations often involve large transactions, and a robust payment gateway can streamline these.

- Freelancers and consultants: Individual service providers can use payment gateways to facilitate easy payment for their services, often through invoicing platforms that integrate a payment gateway.

- Food and beverage industry: Restaurants and cafes offering online ordering can make the process more efficient with an integrated payment gateway.

What are the Cheapest Payment Gateways?

The most affordable payment gateways are:

| Payment Gateway | Transaction Fees (UK Cards) | Transaction Fees (EU/Non-UK Cards) | Other Costs | Contract Length | Learn More |

|---|---|---|---|---|---|

| Stripe | 1.5% + 20p | 2.5% + 20p | None | Month-to-month | Visit Stripe |

| Square | 1.4% + 25p | 2.5% + 25p | None | Month-to-month | Visit Square |

| Worldpay | 0.75% – 2.75% (Sliding Scale) | Same as UK Cards | £9.95 minimum monthly fee | 18-month contract | Visit Worldpay |

It’s worth noticing cheaper transaction rates are often available for businesses willing to commit to long-term contracts or those processing a high volume of transactions per month.

What Makes the Best eCommerce Payment Gateway Service?

There’s no single “best” eCommerce payment gateway service, as the ideal choice depends on your specific needs and priorities. However, there are some key factors that make a great gateway:

- Security and Reliability: Robust fraud prevention features, PCI compliance for data protection, Reliable uptime to prevent sales disruptions

- Features and Functionality: Acceptance of various payment methods (credit cards, debit cards, wallets), Support for recurring billing (subscriptions), International payment options, Mobile-friendly checkout, Transaction data insights for informed decisions

- Ease of Use and Integration: Easy setup and integration with your eCommerce platform, User-friendly interface for smooth customer checkout, Multilingual support for international customers

- Pricing and Fees: Transparent fee structure without hidden charges, Competitive rates (transaction and monthly fees), Potential volume discounts for high-volume businesses

- Additional Considerations: Responsive customer support, Reputation and brand reliability, Scalability to accommodate business growth

Payment Gateway vs. Payment Processor

While the terms ‘payment gateway’ and ‘payment processor’ are often used interchangeably, they refer to distinct components of the electronic payment ecosystem.

Payment Gateway: A payment gateway is a digital conduit that connects your online store or POS system to the payment processing network. It’s essentially the online equivalent of a physical card terminal. The gateway securely transmits payment information from the customer to the payment processor. It encrypts sensitive card details to ensure safe passage of data over the internet. A key feature of a payment gateway is its ability to integrate with various e-commerce platforms and shopping carts, facilitating a smooth and secure online payment experience for both merchants and customers.

Payment Processor: The payment processor, on the other hand, is the backbone of the transaction process. It’s a service that works behind the scenes to handle the actual processing of payments. Once the payment gateway sends the transaction data, the processor communicates with the customer’s bank and the merchant’s bank to approve or decline transactions based on the availability of funds and fraud rules. Payment processors maintain relationships with card associations and are responsible for settling transaction funds, ensuring that the money moves from the customer’s account to the merchant’s account.

Key Differences:

- Function: The gateway is the messenger that securely forwards payment information, while the processor is the system that actually executes the transaction.

- Integration: Payment gateways are designed to integrate with online platforms, whereas payment processors operate in the background and are typically unseen by the merchant or customer.

- Security: Gateways focus heavily on encrypting and securely transmitting data, whereas processors deal with the financial institutions directly for the approval and settlement of transactions.

Alternatives to Using a Payment Gateway

If a traditional payment gateway doesn’t align with your business requirements, there are other financial technology solutions to consider. Peer-to-peer payment systems, direct debit services, and cryptocurrency payment platforms are among the alternatives.

While these may not offer the full range of features that dedicated payment gateways provide, they can offer specific advantages such as lower fees or faster transactions, depending on your business needs.

- Cryptocurrency Processors: Platforms like BitPay or Coinbase Commerce allow merchants to accept cryptocurrencies like Bitcoin or Ethereum. These services often charge lower fees but require both merchants and consumers to be comfortable with digital currencies.

- Direct Bank Transfer Systems: Solutions such as GoCardless or Bacs in the UK facilitate direct debit payments from a customer’s bank account to the merchant’s account. This method is often used for subscription-based services.

- Cheque Payments: Although increasingly uncommon, some businesses still accept cheques as a form of payment. This method is often used for B2B transactions.

- Bank Transfers: Direct transfers from one bank account to another can be arranged without the involvement of a dedicated payment processor. However, this method is often cumbersome for routine retail transactions.

- Escrow Services: These are third-party services that hold funds until goods or services are delivered, commonly used in freelance or contract work.

- Money Order: Similar to cheques but more secure, money orders are often used for larger transactions and are common in the real estate industry.

- Layaway Plans: Some retailers offer layaway plans that allow customers to reserve a product by paying a small deposit, then paying off the balance over time before receiving the product.

Which payment gateway provider is right for me?

Where Do Your Customers Shop?

If you sell more online than in person, or vice versa, this affects your choice. Some gateways are better for online sales, others for in-person. Also, the cost can vary based on how your customers are paying – online or face-to-face.

How Do Your Customers Like to Pay?

Do your customers prefer using credit cards or digital wallets like Apple Pay or Google Wallet? Your choice should support the payment methods your customers use most. Some gateways offer better deals or features for certain payment types.

What’s Your Sales Volume?

Look at how much you sell each month. If your sales are high, a gateway with a monthly fee but lower transaction costs might save you money. If your sales are lower, a gateway with no monthly fee but higher transaction costs could be better.

What are the Setup and Maintenance Requirements?

Assess the ease of setting up and maintaining the gateway. Some gateways may require technical expertise to integrate, while others might offer simple, user-friendly setup processes.

Is There Flexibility for Growth?

Consider whether the gateway can scale with your business. As your business grows, your payment processing needs might change.

Are There Any Restrictions or Limitations?

Some gateways might have restrictions on certain product categories or impose limits on transaction sizes. Ensure the gateway you choose aligns with your business model.

What’s the Customer Experience Like?

A smooth and straightforward checkout process can help reduce cart abandonment. Evaluate the customer experience from start to finish.

Payment Gateway FAQs

Payment gateways typically use one of three methods for multi-currency transactions:

- Real-time Conversion: Immediate conversion of customer’s payment into the merchant’s currency.

- Separate Currency Accounts: Merchants hold different accounts for each accepted currency, depositing foreign payments accordingly.

- Hybrid Approach: A combination of immediate conversion and separate accounts, usually segmenting the transaction amount.

Tokenisation replaces sensitive card details with a unique identifier or “token,” thereby safeguarding financial information during transactions. This significantly reduces the risk of data breaches and unauthorized access.

Dynamic pricing adjusts the cost based on real-time market conditions, seasonality, or customer behaviour. This variability can introduce complexities in payment processing, such as the need for real-time data analytics and adaptable transaction handling mechanisms.

A chargeback occurs when a customer disputes a transaction, leading to the reversal of the payment. Frequent chargebacks can result in higher processing fees and even termination of your payment gateway service.

Payout schedules refer to the frequency with which the payment gateway transfers collected funds to the merchant’s bank account. Variability in this schedule can affect your cash flow, requiring strategic planning around revenue cycles.

While fees for payment processing might seem minimal per transaction, they can accumulate and significantly impact your profit margins. It’s important to understand the fee structure of your payment gateway and plan accordingly.

Compliance with security protocols such as PCI DSS (Payment Card Industry Data Security Standard) is mandatory for payment gateways. Failure to comply can result in severe penalties and may jeopardize your ability to process payments.

Payment gateways commonly utilize fraud detection features like machine learning algorithms and behavioural analytics. These tools aim to flag suspicious activities, thereby mitigating the risk of fraudulent transactions.

Payment gateways commonly utilize fraud detection features like machine learning algorithms and behavioural analytics. These tools aim to flag suspicious activities, thereby mitigating the risk of fraudulent transactions.

The uptime of a payment gateway—the time it is fully operational—directly affects your ability to complete transactions. A gateway with frequent downtimes can result in lost sales and eroded customer trust.