Founded in 2007, West One is a specialist lender that offers bridging loans, development finance, buy-to-let mortgages, and more.

The lender is particularly known for serving clients who might not fit the traditional criteria for high street lenders, making them a popular choice for developers, investors, and landlords in need of alternative lending solutions.

West One aims to offer flexibility in their lending, and they have built their reputation by addressing the needs of specific niches within the lending market. They often focus on projects and clients that may be considered higher risk by traditional standards but can still be viable with the right lending structure.

In this review, I will take a closer look at West One, including its products and features, services, rates, and reviews. I will also discuss the lender’s financial stability and its overall reputation.

This review will be heavily focused on West One’s bridging loan products.

West One Bridging

West One offers regulated and unregulated bridging loans from £75k to £30m for both residential, commercial and land projects. These can be used to quickly secure property purchases, fund refurbishments, raise capital, or refinance existing loans.

Key Features Include

- Bridging Loans from £75k to £30M (Higher may be considered)

- 1st and 2nd charge loans available

- Loans secured against all property types

- Rates start from 1.00% per month for terms up to 24 months

- Max LTV up to 75%

- Minimum term of 1 month

- No early repayment charges

- Complex offshore structures are considered

Overall, West One has a great reputation, especially if you’re looking to finance an atypical or riskier project. The application process is quick and easy, and West One seems to really put the accent on timing to provide fast financing.

What are the Eligibility Criteria for a West One Bridging Loan?

West One Residential Bridging – Regulated

| Criteria | Value |

|---|---|

| Eligible Property Type | Residential Only |

| Charge Type | 1st & 2nd |

| Minimum Loan Size | £75k |

| Exit Strategy | Evidence of a Robust Exit Strategy |

| Residency Type | Primary Place of Residence |

| Minimum Age | 18 |

| Maximum Age | ❎ |

| Location | England, Wales and Mainland Scotland |

| Minimum Term | 1 Month |

| Maximum Term | 12 Months |

| Interest | Retained Only |

West One Residential Bridging – Unregulated

| Criteria | Value |

|---|---|

| Eligible Property Type | Residential Only |

| Charge Type | 1st & 2nd |

| Minimum Loan Size | £75k |

| Exit Strategy | Evidence of a Robust Exit Strategy |

| Residency Type | Investment properties only |

| Minimum Age | 18 |

| Maximum Age | ❎ |

| Location | England, Wales and Mainland Scotland |

| Minimum Term | 1 Month |

| Maximum Term | 24 Months |

| Interest | Retained / Serviced Only |

West One Semi-Commercial and Commercial Bridging

| Criteria | Value |

|---|---|

| Eligible Property Type | Places of worship, schools, football clubs or operating care homes are generally not acceptable |

| Charge Type | 1st and 2nd |

| Minimum Loan Size | £75K |

| Minimum Age | 18 |

| Maximum Age | ❎ |

| Location | England, Wales and Mainland Scotland |

| Minimum Term | 1 Month |

| Maximum Term | 24 Months |

| Interest | Retained / Serviced Only |

West One Land Bridging

| Criteria | Value |

|---|---|

| Charge Type | 1st |

| Minimum Loan Size | £75K |

| Minimum Age | 18 |

| Maximum Age | ❎ |

| Location | England, Wales and Mainland Scotland |

| Minimum Term | 1 Month |

| Maximum Term | 24 Months |

| Interest | Retained / Serviced Only |

Application Process for West One Bridging

The application process for a bridging loan with West One is straightforward. Just like many financial services, you’ll start by filling out a form with your personal details.

Once that’s submitted, an expert from their team will get in touch with you to discuss the specific terms of the loan. It ensures that every client’s individual needs are addressed with precision.

I do wish they had a calculation tool or a fast-track application page on their website for a more immediate understanding and quicker processing. It would have been a useful feature for those seeking instant estimates or a streamlined application experience.

West One Bridging Rates & Fees

Here are the West One bridging loan rates for 2023.

| Loan Type | Rate | Max. LTV | Main Requirement |

|---|---|---|---|

| Regulated Residential Bridging | from 1.00% – 1st charge from 1.05% – 2nd charge | 1st charge – 70% 2nd charge – 65% | Evidenced, Robust Exit Strategy |

| Unregulated Residential Bridging | from 1.00% – 1st charge from 1.05% – 2nd charge | 1st charge – 70% 2nd charge – 65% | Evidenced, Robust Exit Strategy |

| Semi-Commercial Bridging | from 1.00% – 1st charge from 1.05% – 2nd charge | 1st charge – 70% 2nd charge – 65% | Proof of Funds / Evidence of Deposit |

| Land Bridging | from 1.10% | With planning – 65% Without planning – 50% | Proof of Funds / Evidence of Deposit |

When taking a bridging loan with West One, you might encounter the following fees.

| Fee | Description | Amount |

|---|---|---|

| CHAPS Fee | Electronic transfer of the mortgage funds | £35.00 |

| Duplicate Fee | Requesting a copy of a previous loan statement or an interim statement of your account as it stands | £25.00 |

| Giving You a Reference | Another lender asks for a loan reference, such as how you have managed your loan account with West One | £50.00 |

| Unpaid Ground Rent / Service Charge Fee | Failing to pay your ground/chief rent charges or service/maintenance charges | £100.00 |

| Arrears Fee | Charged each month while your arrears equal to or greater than one month’s full payment | £60.00 |

| Over-Term Fee | Charged for each month your loan goes beyond the loan end date. | £250.00 |

You can consult the full list of West One fees and charges here.

West One Reviews & Ratings

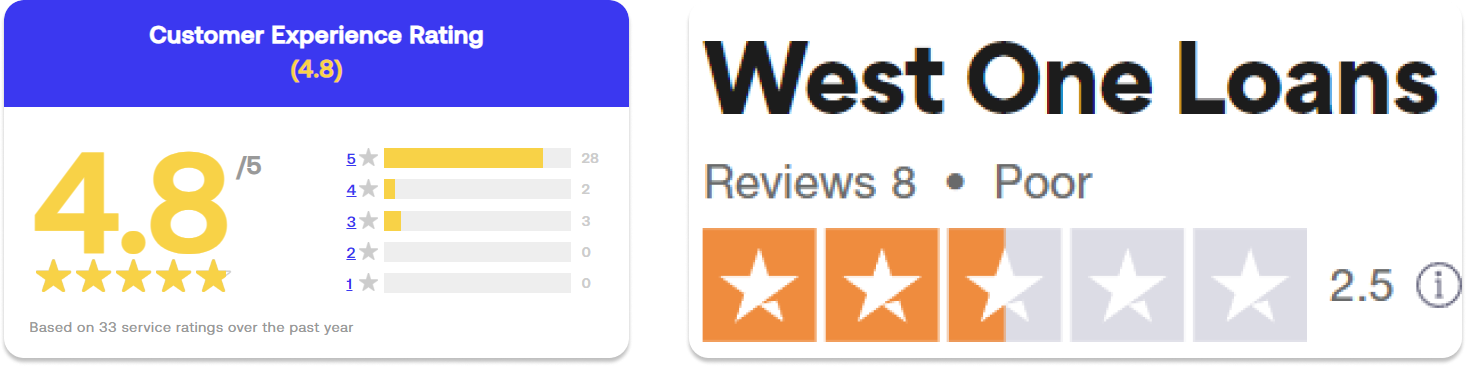

West One receives really mixed reviews, and the overall customer satisfaction seems to shift quite a lot.

On feefo, West Loans gathers 213 comments, with an average rating of 4.6 out of 5 stars. Very positive reviews praise excellent customer service, helpful staff, and fast loan processing times. A few negative reviews mention high-interest rates or issues contacting customer support

The situation is radically different on Trustpilot. West One gets an average rating of 1.4 out of 5 stars. Many negative reviews complain about poor customer service, misleading information, and unexpected fees and charges. Some other issues include difficulty contacting support, problems with repayments and access to accounts, and lack of transparency with fees. Some positive reviews highlight good service, but the majority seem dissatisfied.

However, keep in mind that a negative impression might be based on the low amount of reviews. It’s a good idea to consider the number of reviews before making a judgment.

Compare bridging loans

Save time and money with Business Expert & Fluent Bridging

Quick Search – Compare bridging loan criteria in real time

Easy Process – Answer a few quick questions about your loan needs

Expert Support – Get access to our partner’s in-house advisers

West One FAQs

How does West One ensure a smooth process for bridging loan applicants?

West One has an experienced underwriting team that provides the needed speed and flexibility to help get clients’ projects over the line when timing is critical.

What types of properties can be used as security for West One bridging loans?

Bridging loans from West One can be secured against various properties, including residential, commercial, semi-commercial properties and land. The loans can be used for purchases, refurbishments, or refinances of these properties.

Can businesses benefit from West One’s commercial bridging loans?

Yes, businesses can use commercial bridging loans from West One to cover short-term cash flow issues, finance tax liabilities, or even as working capital. New businesses can also use them as a cash flow injection to acquire additional stock, new equipment, or premises for the business.

What are the eligibility criteria for a commercial bridging loan from West One?

To qualify for a commercial bridging loan, the overall use of the property as collateral must be at least 40% commercial. Most lenders, including presumably West One, would also insist on a separate entrance to any residential part of the property.

Can private landlords use West One’s commercial bridging loans?

Yes, private landlords can use commercial bridging loans from West One for renovations to improve rental yields, which enhances the properties value. This makes it easier for landlords to refinance them onto competitive Buy-to-Let (BTL) mortgages and clear any bridging.