Moneyfarm is a leading digital wealth management platform designed to help you invest your money in a simple, affordable, and efficient way.

Its investment strategy is based on a low-cost, passive approach, with the goal of low fees and minimal exposure to market volatility.

Over 90,000 investors currently choose it for its simplified approach to investing.

It’s part of a new breed of investment digital wealth manager apps (robo advisors) that do it all for you, with no prior experience needed.

My independent review will delve into how Moneyfarm manages investments, explore its charges and fees, and evaluate its performance and portfolio returns. I’ve been using an account for several months as part of a deep dive into its functionality.

Should you use it? Let’s find out…

- My Verdict

- Pros and Cons

- Who is Moneyfarm?

- How Does Moneyfarm Work?

- Understanding Moneyfarm Investment Portfolios

- What’s Moneyfarm’s Investment Process?

- Account Options

- How does Moneyfarm manage your portfolio?

- Performance: What’s the average return?

- Ways to Invest

- Eligibility

- How to Open an Account

- Moneyfarm Fees & Charges

- Security

- App Review

- What’s the customer support like?

- Customer Reviews

- Alternatives to Moneyfarm

- FAQs

Moneyfarm Review: My Verdict

Moneyfarm is simple, safe, well-priced and with a good track record for its investments: I’ve been impressed with this handy and effective way to invest your money.

I found the user experience superb, and the fact that you can speak with a real person via the app or phone separates them from a platform like Nutmeg, which is not permitted to offer advice.

By my analysis, the company’s solid performance track record and diverse portfolio options make it a viable choice for investors of varying risk appetites.

Although the minimum entry of £500 may put off some, this is an overall excellent investing platform and one which, based on my experience, deserves its strong reviews and wide user base.

Pros and Cons of Moneyfarm

Pros

- A simplified fee structure that is not expensive (0.25-0.75%).

- Choice of actively managed, fixed allocation, or socially responsible portfolios.

- Option to receive regulated advice from an Investment Consultant.

- Regulated by the UK Financial Conduct Authority (FCA)

- Investments protected by Saxo Bank

- Positive customer reviews and industry recognition

Cons

- The minimum investment requirement of £500 may be a barrier for some.

- Limited control over specific assets compared to a regular investment platform

- App can be slow to load at times

- Some clients report waiting times for customer support during peak hours

Who is Moneyfarm?

Moneyfarm is a leading pan-European digital wealth management platform, catering to over 100,000 active investors and managing more than £2.6 billion in assets.

Established in 2011, Moneyfarm’s mission is to simplify and make personal investing accessible to a wider audience by leveraging technology. .

The company has won prestigious awards such as the UK’s “Best Online Direct to Consumer Investment Platform” and “Innovation of the Year.” It has offices in offices in Milan, London, and Cagliari.

Its board of directors includes some major names in business, such as Chair Dame Jayne-Anne Gadhia, brings extensive expertise and leadership from institutions such as Snoop, Virgin Money, and Allianz. Moneyfarm’s investors and advisors, including M&G, Allianz, Poste Italiane, United Ventures, and Cabot Square Capital.

How Does Moneyfarm Work?

Moneyfarm operates on a passive investment strategy, whereby instead of actively selecting stocks or timing the market, it allocates your funds across a diverse array of assets such as stocks, bonds, and cash.

This strategy offers two key advantages:

- Cost-effectiveness: With its nominal fees, Moneyfarm ensures a larger proportion of your money remains invested, thereby potentially yielding higher returns for you.

- Risk Mitigation: Through a diversified portfolio, Moneyfarm aims to lessen the inherent risk associated with investment. By spreading your investment across different asset classes, it reduces the potential impact of any single asset class underperforming.

Beginning your investment journey with Moneyfarm involves responding to a few queries regarding your investment objectives and risk appetite. Based on your responses, Moneyfarm devises a personalized investment portfolio, with the flexibility to adapt as your circumstances evolve.

In my experience, setting up the portfolio was swift, clocking in under five minutes, making it one of the quickest onboarding processes among the platforms I have explored.

Speak with a Real Moneyfarm Investment Consultant

One of the things I like best about Moneyfarm is that it gives the chance to leverage the expertise of a personal investment advisor. From my perspective as a seasoned finance professional, this is a service that offers substantial value.

You can phone, email, chat online or even meet face to face to discuss anything from portfolio selection, performance or even retirement planning, drawdown support, and pension consolidation.

Understanding Moneyfarm Investment Portfolios

Moneyfarm has tailored a selection of nine model portfolios to cater to varying levels of risk tolerance.

These portfolios meet the needs of a wide array of investors, from those cautious about risk to those who are more open to higher-risk ventures.

Grounded in a risk-based asset allocation model, each portfolio is designed to reflect the investor’s age, financial goals, and risk appetite, ensuring an automatic rebalancing that aligns with the investor’s risk parameters.

Composed of a diversified mix of assets, including stocks, bonds, and cash, the portfolios provide a broad base for reducing risk and mitigating volatility. These portfolios are actively managed by a team of seasoned investment professionals to continuously serve the best interests of the investors.

In order to select these model portfolios, Moneyfarm employs a statistical technique known as Value at Risk (VaR). VaR provides an estimate of the maximum loss an investor can anticipate within a specified level of confidence.

Moneyfarm uses this measure to calculate the likelihood of similar losses occurring between two portfolios. If this probability exceeds 95%, the allocation is not considered for the model portfolio.

However, if the probability falls below 95%, the allocation is included within the investable universe, indicating that it has the potential for inclusion in a model portfolio. This rigorous selection process helps ensure that the portfolios align with the investors’ risk tolerance and investment objectives.

What’s Moneyfarm’s Investment Process?

Moneyfarm’s investment process is a three-step process that begins with forming long-term expectations for risk and returns for each asset class. The second step is to combine these expectations to create a set of portfolios (one for each risk profile), called Strategic Asset Allocation (SAA).

Finally, the Tactical Asset Allocation (TAA) adjusts the SAA to reflect Moneyfarm’s tactical view.

The SAA is based on long-term assumptions, while the TAA takes into account shorter-term factors, such as economic cycles and market sentiment. The goal of the TAA is to reduce the risk of the portfolios while still maintaining the potential for long-term growth.

Moneyfarm uses a variety of factors to determine the TAA, including:

- Fundamental considerations include factors such as the global economy, the business cycle, and the starting expectations for each asset class.

- Recent developments: This includes factors such as economic, political, and policy-related developments.

- Loss aversion: Moneyfarm takes into account the loss aversion of its customers, which means that the TAA is designed to reduce the probability of large losses.

The TAA is reviewed and adjusted on a regular basis, typically every quarter. This ensures that the portfolios are always aligned with Moneyfarm’s investment views and the risk tolerance of its customers.

Overall, Moneyfarm’s investment process is a well-diversified and risk-managed approach to investing.

The SAA provides a long-term framework for investing, while the TAA helps to reduce risk and volatility. These two approaches are designed to help investors achieve their long-term financial goals.

What are Different Moneyfarm Account Options?

Moneyfarm Stocks & Shares ISA Review

Moneyfarm’s Stocks and Shares ISA, offers the standard tax-free returns on up to £20,000 each and every year. If you have an existing ISA elsewhere, transferring is easy and won’t cost you a penny.

Its benefits include:

- Access and Control: Withdrawing and reinvesting up to your annual ISA limit is without penalties.

- Supportive Investment Consultants: One of Moneyfarm’s core strengths is the personal touch they offer. They have a team of investment consultants who are available for customers, providing guidance and advice.

- ISA Transfers: With a straightforward process and friendly customer support, Moneyfarm makes the process of transferring existing ISAs a breeze.

- Value for Money: Moneyfarm’s low fee structure ensures that your hard-earned money is put to work effectively.

- Personalised Investments: Based on your investment profile, goals, and risk appetite, Moneyfarm’s team creates a portfolio tailored to your needs.

- Transparent Pricing: Moneyfarm follows a single, easy fee structure with no hidden costs.

- Projection Tools: Their comprehensive tools provide you with projected values of your portfolio over time, considering different levels of contributions and risk levels.

Moneyfarm General Investment Account

Moneyfarm’s General Investment Account (GIA) offers a flexible and limitless way to invest. You’re free to contribute as much as you want, making it a great choice if you’ve maxed out your annual ISA allowance. It also provides flexible access to your funds without additional withdrawal fees.

In terms of planning and advice, you’re not alone. Moneyfarm’s team will help you design a plan around your goals, and you can communicate with them through chat, phone, or email.

You can open a separate portfolio for each of your goals, even with varying risk levels. This versatility allows you to tailor your investments to specific needs and aspirations. The portfolios are managed by Moneyfarm’s expert team, who carefully track market trends, build, manage, and rebalance your portfolio for you.

Fees for Moneyfarm’s GIA are competitive. As you save and invest more, you pay less in fees, allowing you to keep more of your returns.

Interested in seeing potential growth? Moneyfarm allows you to explore different investment plans and visualize your expected future growth. They provide a handy calculator where you can input your initial deposit, monthly contribution, time frame, and risk level to estimate your future wealth.

Moneyfarm is committed to transparency in their fees. The more your money grows, the lower the percentage of your fees. For balances below 100K, fees range from 0.75% to 0.60%. Above 100K, fees drop to a range between 0.45% and 0.35%.

Getting started is easy. Moneyfarm guides you in discovering your investor profile, opens your recommended portfolio, and then invest when you’re ready.

Moneyfarm SIPP Review

The Moneyfarm Self-Invested Personal Pension (SIPP) offers an adaptive approach to portfolio management, reducing risk as your target retirement date approaches. Upon reaching 55, you have the option to withdraw up to 25% of your pension tax-free, either in one lump sum or in instalments. Importantly, your pension funds can be passed on to your beneficiaries free of inheritance tax.

A valuable aspect of Moneyfarm’s service is the personal investment consultant provided to guide you towards your goals. There’s also the possibility of consolidating pensions and setting up employer contributions for more straightforward growth monitoring.

Moneyfarm facilitates the pension transfer process, aiming for a smooth, paperless experience. This typically takes between 3-4 weeks, subject to your existing provider’s policies. To initiate a transfer, you would need to provide your current provider’s name, pension account number, pension value, and the valuation date.

Their fee structure is relatively simple and decreases as your investment grows. Fees for actively managed funds range from 0.75% for amounts below £10K, dropping down to 0.35% for amounts above £500K.

Moneyfarm Junior ISA

Moneyfarm provides a Junior Individual Savings Account (JISA) aimed at giving children a financial head start. The annual deposit limit is set at £9,000, which can be invested in a sustainable manner, if desired.

The Junior ISA could be used for purposes like financing a first house, university tuition, or simply to help them pursue their dreams. If you save just £750 per month, your child’s Junior ISA is projected to be worth over £280,000 when they turn 18.

The investment strategy for Junior ISAs at Moneyfarm aligns with their Classic and Socially Responsible portfolios, providing a long-term plan for maximizing the growth of the investment. All returns are protected from income and capital gains tax, making a Junior ISA a long-term, tax-free, and efficient savings option.

Transferring an existing Junior ISA to Moneyfarm is straightforward. Their team assists in the process, setting up the account and handling the transfer from the current JISA provider. They also offer smart tech tools to monitor the performance of your JISA from anywhere and a dedicated team of investment consultants for assistance.

One can automate monthly deposits to never miss an investment opportunity and even encourage third-party contributions. Friends and family can be encouraged to contribute to your child’s financial future by directly depositing money into the JISA.

The fee structure at Moneyfarm is simple and tiered based on the investment amount. Below £100,000, the fees range from 0.75% for £500 to 0.60% for £50,000. Above £100,000, the fees decrease from 0.45% to 0.35% for larger investment amounts.

Features of a Moneyfarm Junior ISA include the option for third-party contributions, on-hand investment consultants, a long-term strategy with the possibility of investing up to £9,000 per tax year, sustainable portfolios backed by MSCI data, simple and transparent fees, and tax-free investing.

How does Moneyfarm manage your portfolio?

Moneyfarm adopts a systematic, data-driven approach to managing your portfolio, aiming to align with your financial goals, knowledge, and risk tolerance. This methodology combines human expertise with cutting-edge technology to optimize your investment journey.

- Personalization: Your investment journey begins with understanding your goals, your knowledge of financial matters, and your attitude towards risk. This information is crucial to build a portfolio that’s aligned with your financial aspirations.

- Diversification: Moneyfarm uses a globally diversified mix of assets such as global equities, corporate bonds, and commodities. This approach is designed to maximize returns in line with your attitude towards risk. Depending on your risk tolerance, your portfolio may be more heavily invested in stocks or bonds.

- Risk Mitigation: Moneyfarm utilizes Exchange Traded Funds (ETFs) for an additional layer of diversification to protect your portfolio from the volatility that individual stocks may experience.

- Evidence-Based Decisions: Every decision at Moneyfarm is data-driven, guided by both quantitative techniques and qualitative judgement. Their investment committee oversees the whole process.

- Future Anticipation: The strategic asset allocation team looks at a 10-year horizon, predicting each asset class’s expected returns and volatility. They consider how these assets might react to future economic and political developments.

- Balancing Short and Long-Term Views: Moneyfarm’s investment committee focuses on balancing a long-term perspective with a one-year tactical asset allocation strategy. This approach takes advantage of short-term market opportunities when they arise.

- Portfolio Management Options: You have the choice between fixed allocation and actively managed portfolios. Fixed allocation portfolios follow the market trends, while actively managed portfolios benefit from constant monitoring to optimize performance and reinvest dividends.

Moneyfarm Performance: What’s the average return?

As a potential investor on Moneyfarm, the performance is likely to be one of your most important questions. How do their investment managers actually perform? What kind of return are you going to see on your investment?

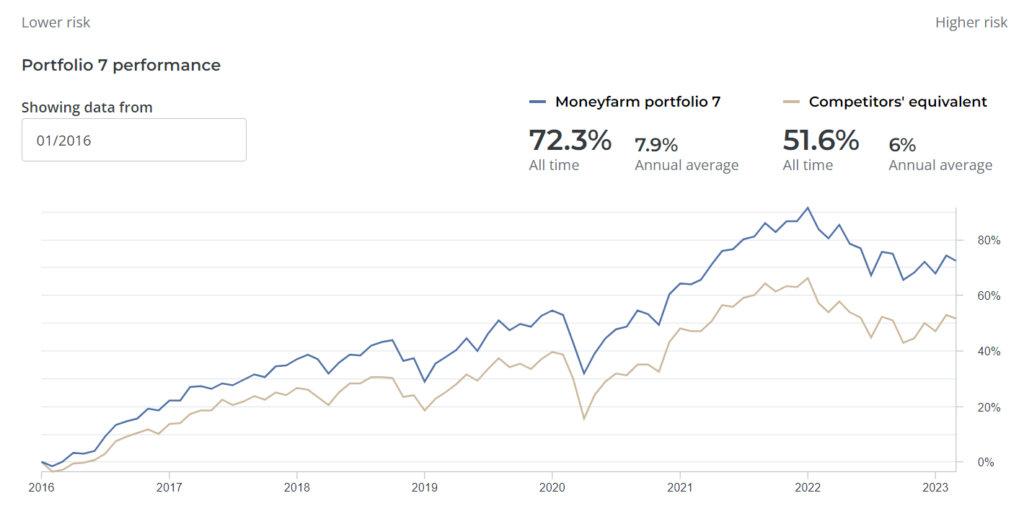

Moneyfarm offers 7 specifically designed portfolios and, based on the answers to the questions you submit in the initial questionnaire, you’ll be assigned one of these.

You can see all of the historical results for each of these of their website. Average returns have been as follows:

- 2022 = 12.4%

- 2021 = 16.4%

- 2020 = 6.1%

- 2019 = 19.8%

- 2018 = -5.9%

- 2017 = 12.3%

- 2016 = 22.1%

As you can see from the screenshot below (from their website) their performance against competitors is strong, and well above average.

Moneyfarm vs Nutmeg Performance

For most prospective users of Moneyfarm, the key competitor would be someone like Nutmeg, one of the U.K.’s biggest robo-advisors, with assets under management of over £3.5 billion.

I’ve compared the Moneyfarm performance figures with those of Nutmeg, and I can see they are broadly comparable. Moneyfarm outperforms Nutmeg on some of its mid range portfolios whereas Nutmeg wins on both the lowest risk and highest risk portfolio choices.

One interesting thing to note is that Nutmeg did perform surprisingly well during the last few years, a tougher economic period for most investors.

Overall, there’s very little in it. I note that Moneyfarm is cheaper if you’re investing more than £10k, plus you have the option to book a call with an investment consultant without paying anything extra.

Ways to Invest on Moneyfarm

Moneyfarm Active Management

When you opt for active management, your investments are regularly reviewed and adjusted to capitalize on market opportunities while staying within your comfort zone. This strategy aims to outperform the market rather than just follow it.

Here’s how active management works at Moneyfarm:

- Creating an Investor Profile: The first step involves understanding your investment goals and risk tolerance. You answer a few simple questions about yourself, your financial goals, and your attitude towards investment. This helps Moneyfarm to create your investor profile. If your goals or other factors change, your profile can be quickly adjusted online or via their app.

- Portfolio Matching: Once you’ve chosen active management and decided on a product (e.g., an ISA), Moneyfarm matches your investor profile with a diversified portfolio composed of a mix of handpicked, cost-efficient ETFs. Each portfolio is designed to meet Moneyfarm’s high standards of quality and reliability.

- Portfolio Management: After you fund your portfolio, your investments are actively managed under the day-to-day direction of your Chief Investment Officer, Richard Flax, and Moneyfarm’s investment committee. Unlike fixed allocation portfolios, which are rebalanced once per year, actively managed portfolios are regularly rebalanced to seize market opportunities and align with your investment profile.

- Dedicated Consultant: Alongside the active management of your portfolio, you also get access to a dedicated investment consultant. This consultant is available to chat whenever you need, providing support and answering your questions about your portfolio, the wider market, or your investment plan.

Choosing active management can be beneficial if you are comfortable with a higher degree of risk and want to potentially achieve higher returns by capitalizing on market trends.

Moneyfarm Environmental, Social, and Governance (ESG) investing (ESG)

Moneyfarm offers a distinct service called Environmental, Social, and Governance (ESG) investing that aligns your investment portfolio with your world view. The ESG investment strategy includes investing in companies that meet specific criteria related to environmental responsibility, social practices, and corporate governance.

Here’s how it works:

- Aligning Your Investments with Your Values: Moneyfarm allows you to invest in a socially responsible portfolio that supports forward-thinking initiatives. These could be companies that are switching to renewable energy, hiring diverse minds at board level, or addressing social and environmental challenges.

- Understanding Your Impact: Moneyfarm’s socially responsible portfolios are designed using funds invested in some of the world’s most forward-thinking and impactful companies. These portfolios are assessed based on MSCI data, which helps ensure that the selected ESG funds meet certain standards. For example, the mid-range ESG portfolio offered by Moneyfarm has significantly lower carbon emissions and 100% compliance with the United Nations Global Compact and Labour laws.

- Targeting Sustainable Growth: Moneyfarm’s ESG portfolios aim to provide returns similar to those of non-ESG portfolios. They are diversified across different asset classes and are designed to deliver long-term, sustainable growth. The funds are selected and monitored using standard MSCI metrics and direct communication with ETF issuers.

- Active Engagement: In addition to the standard metrics, Moneyfarm has an ESG Engagement Layer that measures how actively asset managers engage with fund issuers and their organisations. This could include voting to drive positive change within an organisation or monitoring outcomes.

- Fees: Just like their other services, Moneyfarm has a tiered fee structure for ESG portfolios based on the amount of money you invest. As your investment grows, the percentage of your fees decreases.

To start investing in an ESG portfolio with Moneyfarm, you first need to create your investor profile. After understanding your attitude towards investing and your investment goals, Moneyfarm matches you with a globally diversified ESG portfolio that fits your needs, goals, and values. Once you’re ready, you can transfer your existing account or add funds to start investing.

ESG investing is a good choice if you wish to align your investment strategy with your personal values and ethical beliefs.

Moneyfarm Thematic Investing

hematic investing on Moneyfarm is a unique investment approach that allows you to invest in long-term global trends that are set to shape the future. This investment strategy is centered around the creation of a portfolio that mirrors certain themes or trends such as technology, sustainability, society, and multi-trends.

There are several reasons why you might choose thematic investing with Moneyfarm:

- Exposure to Long-Term Global Trends: Thematic investing at Moneyfarm gives you the opportunity to invest in sectors like technology (semiconductors, e-commerce, electric vehicles, clean energy, artificial intelligence), sustainability (circular economy, clean energy, blue economy, clean water), society (e-commerce, esports, global infrastructure, gender equality), and multi-trends (e-commerce, semiconductors, global infrastructure, circular economy). These themes are carefully selected to capture growth from long-term trends and disruptive innovations.

- Risk Management: Thematic investing at Moneyfarm also uses a core-satellite approach. Your portfolio is divided into two parts: the “core” or your base portfolio, and the “satellite”, consisting of your choice of growth themes. The core is made up of low-cost, broad-based index funds and ETFs, while the satellite contains targeted, high-growth investments that align with broader long-term trends. This approach aims to balance risk by combining the stability of a diversified core with the growth potential of thematic investing.

- Personalization: With Moneyfarm, you can select the growth themes that best align with your values and add them to your new or existing portfolio. You’re given the control to decide how much of your portfolio you want to dedicate towards your selected growth themes.

- Access to Expertly-Built Growth Themes: Moneyfarm’s expertly-built growth themes are designed to enhance your portfolio and give it the potential for greater long-term performance. They focus on companies providing solutions to global challenges, aiming to deliver better outcomes not just for investors, but for everyone.

- Access to Renowned Fund Managers: Moneyfarm’s thematic investing gives you access to ETFs from some of the best fund managers in the world, giving you the confidence that your investments are being managed professionally.

In conclusion, if you are interested in investing in the megatrends that are changing the world and shaping our future, and you want a diversified and risk-managed portfolio, then thematic investing at Moneyfarm could be a suitable choice for you.

Moneyfarm Fixed Allocation

Fixed allocation investing on Moneyfarm is a type of investment strategy where your portfolio is created with a specific allocation of assets and left to grow over time with minimal intervention. This approach offers a low-cost, passive investing experience, often suited for those seeking long-term growth.

Here are some reasons why you might choose the ‘fixed allocation’ approach with Moneyfarm:

- Passive Investing: A fixed allocation portfolio offers a hands-off approach to investing. It is created by experienced investment experts and then left to grow. Investments are made into diversified assets across the globe, and they move in line with market trends without frequent active intervention.

- Lower Costs: Since this investment strategy involves minimal intervention and only one portfolio rebalance per year, Moneyfarm is able to offer lower cost fixed allocation portfolios. The management fees start from 0.25%, which can be more cost-effective compared to other investing approaches that may involve higher fees for active management.

- Social Responsibility: Much like their actively managed portfolios, Moneyfarm’s fixed allocation portfolios can also be built to align with your values, allowing you to invest in a socially responsible manner.

- Ease of Control: Your money is available and accessible. You can withdraw and reinvest throughout the tax year without penalties. This flexibility might be appealing if you prefer to maintain control of your investments.

- Compatibility with Various Investment Products: The fixed allocation strategy is compatible with a variety of Moneyfarm’s investment products, including Stocks & Shares ISA, Private Pension (SIPP), General Investment Account, and Junior ISA.

However, it’s worth noting that the fixed allocation approach does lack certain elements compared to Moneyfarm’s actively managed portfolios. While you still have access to their dedicated investment consultants and user-friendly app, you’ll miss out on expert active management and regular rebalancing by the asset allocation team who constantly look for new investment opportunities.

In conclusion, the ‘fixed allocation’ approach on Moneyfarm might be ideal if you prefer a low-cost, low-intervention investment strategy, especially if you are planning for long-term growth.

Moneyfarm Eligibility

Moneyfarm is available to residents of the United Kingdom. Investors must be at least 18 years old and have a valid UK bank account.

Additionally, you’ll be required to complete an application form that provides Moneyfarm with necessary information to understand their clients and the source of their funds. Prospective clients must also have the minimum investment amounts required for each product they wish to invest in

How to Open an Account with Moneyfarm

Opening an account with Moneyfarm is a straightforward process that can be completed online.

Potential investors can register on the Moneyfarm website or through their mobile app.

The registration process involves answering a risk assessment questionnaire to determine the suitable portfolio for your investment goals and risk tolerance.

Is it Easy to Withdraw Money from Moneyfarm?

To withdraw your funds from Moneyfarm, you first need to disinvest the desired amount from your investment portfolio. This should be processed within 3 working days: the money then becomes available as cash in your Moneyfarm account.

Once available as cash, you can request a withdrawal to your nominated bank account. Withdrawals are processed within 3 additional working days. So from start to finish, the total time to withdraw is 5-7 working days.

The process seems simple enough through Moneyfarm’s interface and customers are guided along each step. The only complexity is the mandatory disinvestment first before cashing out.

Overall, withdrawing funds from Moneyfarm appears to be a smooth experience that can be completed online in less than a week in most cases. The step-by-step process is clearly outlined and customers are supported along the way. This ease of access to withdraw likely provides customers comfort in using Moneyfarm for investing.

Moneyfarm Fees & Charges

Here are the current fees for Moneyfarm:

- Investment management fee: This is the main fee charged by Moneyfarm, and it covers the cost of managing your investment portfolio. The fee is 0.75% on investments up to £5,000, 0.70% on investments between £5,000 and £10,000, 0.65% on investments between £10,000 and £20,000, 0.60% on investments between £20,000 and £50,000, 0.45% on investments between £50,000 and £100,000, 0.40% on investments between £100,000 and £250,000, and 0.35% on investments over £250,000.

- Underlying fund fees: These are the fees charged by the investment funds that Moneyfarm invests in. The underlying fees vary depending on the fund, but typically range from 0.10% to 0.50%.

- Market spread: This is the cost of buying and selling investments. The market spread is typically very small but can add up over time.

In addition to the platform fees, there are a few other fees that investors may incur, such as:

- Transfer fees: You may be charged a transfer fee if you transfer your investment portfolio from another platform to Moneyfarm. The transfer fee is typically around £75.

- Early exit fees: If you withdraw your money from Moneyfarm within the first 12 months, you may be charged an early exit fee. The early exit fee is typically 0.50% of the amount you withdraw.

Overall, Moneyfarm’s fees are competitive with other robo-advisors. However, it is important to note that the fees can vary depending on the size of your investment portfolio.

| Investment Amount | Actively Managed Fee | Fixed Allocation Fee | Average ETF Fee | Market Spread |

|---|---|---|---|---|

| Up to £10,000 | 0.75% | N/A | 0.20% | Up to 0.10% |

| £10,000 – £20,000 | 0.70% | N/A | 0.20% | Up to 0.10% |

| £20,000 – £50,000 | 0.65% | N/A | 0.20% | Up to 0.10% |

| £50,000 – £100,000 | 0.60% | N/A | 0.20% | Up to 0.10% |

| £100,000 – £250,000 | 0.45% | 0.45% | 0.20% | Up to 0.10% |

| £250,000 – £500,000 | 0.40% | 0.35% | 0.20% | Up to 0.10% |

| Above £500,000 | 0.35% | 0.25% | 0.20% | Up to 0.10% |

For example, if you invest £20,000 in an actively managed portfolio, you’ll pay 0.65% as a management fee, 0.20% as ETF fee, and up to 0.10% due to the market spread effect.

Please note that the ETF fee is not directly deducted from your portfolio but incorporated into the ETF’s daily price. The management fee is separate and is paid directly to Moneyfarm.

Security: How Moneyfarm keeps your investments secure

Can you trust Moneyfarm?

Moneyfarm takes security very seriously. The platform uses a variety of security features to protect customer data, including:

- SSL encryption: All data transmitted between Moneyfarm and its customers is encrypted using SSL, which is a standard security protocol that helps to protect data from being intercepted by unauthorized third parties.

- Two-factor authentication: When customers log in to their Moneyfarm account, they are required to enter a code that is sent to their mobile phone in addition to their password. This helps to ensure that only authorized users can access their accounts.

- Firewalls: Moneyfarm uses firewalls to protect its systems from unauthorized access. Firewalls are software programs that monitor incoming and outgoing network traffic and block any traffic that is deemed to be malicious.

- Regular security audits: Moneyfarm’s security systems are regularly audited by independent security firms to ensure that they are up to date and effective.

In addition to these technical security features, Moneyfarm also has a number of policies in place to protect customer data. For example, Moneyfarm only stores the minimum amount of personal data that is necessary to provide its services, and it destroys any data that is no longer needed.

Moneyfarm is authorized and regulated by the Financial Conduct Authority (FCA) in the UK, providing a level of regulatory oversight and protection for investors.

Any uninvested client money held by Moneyfarm is kept separate from the company’s own funds (Saxo Bank and Barclays), providing an additional layer of protection.

Furthermore, Moneyfarm’s investors are eligible for compensation under the Financial Services Compensation Scheme (FSCS) up to £85,000 in case of the company’s insolvency.

Moneyfarm App Review

Moneyfarm’s mobile app offers a user-friendly interface and intuitive design, which I find a pleasure to use. It is somewhat slow to load on occasion which could be improved.

The app provides access to account information, performance updates, and the ability to make investment decisions. You can’t change your risk profile from the app, however, but have to email them to get this implemented.

It’s also easy to track investments and receive notifications regarding your portfolio’s performance. Overall, the app enhances the user experience and simplifies the investment process.

The Moneyfarm app has received generally positive reviews, with an average rating of 4.2 stars based on 5.65K reviews on Google Play. It has also been downloaded over 100K times on Google Play. On the Apple Store, the app has a higher average rating of 4.7 stars based on 1.7K ratings. Overall, the app seems to be well-received by users on both platforms.

The app includes the following functionality:

- Account overview 📈 – Check total portfolio value, asset allocation, and performance charts.

- Funding 💸- Instantly top up your investment account via bank transfer or card payment.

- Withdrawals 🏦 – Initiate withdrawals from your available cash balance.

- Disinvesting 📉 – Select funds to disinvest and make the cash available for withdrawals.

- Notifications 🔔 – Receive alerts about account activity, portfolio changes, and other updates.

- Tax-efficiency 💰 – Optimize account tax efficiency by adjusting ISA allowances.

- Support 🆘 – Access FAQs, guides, chat support and be able to call/email support staff.

- Security 🔒 – Biometric login, passcode, and other security features to protect your account.

- Simplicity 💡 – Intuitive, user-friendly design for easy navigation and account management.

- Real-time data 🕒 – View updated portfolio value, transactions, and changes as they happen.

What’s the customer support like?

Moneyfarm offers 24/7 customer support via phone, email, and live chat. The customer support team is generally very helpful and knowledgeable, and they are always willing to go the extra mile to help customers.

In addition to the standard customer support channels, Moneyfarm also offers a number of resources to help customers, such as a FAQ section, a blog, and a video library. These resources can be a great way to learn more about Moneyfarm and how to use the platform.

Here are some of the pros and cons of Moneyfarm’s customer support:

Pros:

- Available 24/7

- Helpful and knowledgeable staff

- Willing to go the extra mile

- A variety of support channels

- A number of helpful resources

Cons:

- Waiting times can be long during peak hours

- The FAQ section is not always up-to-date

Moneyfarm Customer Reviews

Moneyfarm has received average feedback from customers, with a rating of 3.7 out of 5.0 on Trustpilot. I note that a year or so ago this was much higher (4.2) so it may be that the recent economic downturns and their impact on performance has left some investors riled.

69% of users give the platform 5 stars which is still fairly high.

Users appreciate the platform’s ease of use, clear website, and good customer service.

Just 6% of users give the platform 1 star, but almost all of these (in the last 6 months) have the chief complaint of poor investment performance.

Alternatives to Moneyfarm

While Moneyfarm provides a compelling investment platform, there are a few alternative options you might wish to consider.

One prominent alternative is Nutmeg, another well-known robo-adviser that offers managed ETF portfolios. Nutmeg has similar features to Moneyfarm, including a range of investment products and a user-friendly interface.

Both of their Trustpilot and app store review scores are broadly comparable, but Moneyfarm comes in a little cheaper overall.

Moneyfarms offer of putting you in touch with a real qualified investment consultant further serves to separate the two platforms.

| Platform | Investment Management Fee | Underlying Fund Fees | Market Spread | Transfer Fees | Early Exit Fees | Range of Investment Options | Level of Personalisation | Ease of Use |

|---|---|---|---|---|---|---|---|---|

| Moneyfarm | 0.75% – 0.35% | 0.10% – 0.50% | N/A | £75 | 0.50% | Wide | High | Medium |

| Nutmeg | 0.65% – 0.45% | 0.15% – 0.45% | N/A | £75 | N/A | Wide | Medium | Medium |

| Wealthify | 0.55% – 0.40% | 0.15% – 0.45% | N/A | £75 | N/A | Narrow | Medium | Medium |

| Scalable Capital | 0.60% – 0.35% | 0.10% – 0.40% | N/A | £50 | N/A | Wide | Low | Medium |

| AJ Bell Youinvest | 0.25% – 0.45% | 0.15% – 0.45% | N/A | N/A | N/A | Wide | Low | High |

Moneyfarm FAQs

Can I trust Moneyfarm?

Regulated by the FCA and with funds protected by the FSCS, Moneyfarm is safe and secure with multiple layers of security and protection for client money.

What happens if Moneyfarm goes bust?

All client assets are ringfenced at Saxo Capital Markets UK Ltd meaning you money and assets would be safe even if Moneyfarm became insolvent.