Who the Card Is Best For

- Limited companies needing a high credit limit up to £250,000, well above typical bank-card caps.

- Businesses that clear the balance monthly and never touch the high carried-balance rate.

- Companies that want cashback or Avios on everyday spend, taken as credit, gift cards or air miles.

- Businesses that spend abroad or pay overseas suppliers, with no FX or ATM fees.

- Companies that do not want to switch business bank account, since no current account is required.

Choose Capital on Tap if you’re a limited company that clears the balance monthly and lacks a suitable bank card option. Not needing an existing business current account is genuinely useful if you bank with a challenger bank.

If you bank with Starling and spend £12,000/month on software, contractors, and ad spend, you need a credit card that Starling itself doesn’t offer. Capital on Tap gives you a £50,000+ line without switching. Clear monthly and earn £1,440/year in 1% cashback.

If you carry balances seasonally or regularly, your offered rate is the decision-maker. Don’t apply without checking your individual rate first.

Eligibility and Application

| Requirement | Capital on Tap rule |

|---|---|

| Business type | Limited company, LLP or PLC |

| Sole traders | Not eligible |

| Partnerships | Not eligible |

| Turnover | £24,000/year (stated on CoT’s comparison page; omitted from its main eligibility page) |

| Company status | Active at Companies House |

| CCJs | No unsatisfied CCJs in the last 12 months |

| Bank account | Existing business bank account required (any UK bank); no switch to CoT needed |

| Personal guarantee | Required from a director or major shareholder |

| Excluded types | High-risk industries, charities, trusts, dormant or dissolved companies |

| Verified 23 July 2026. | |

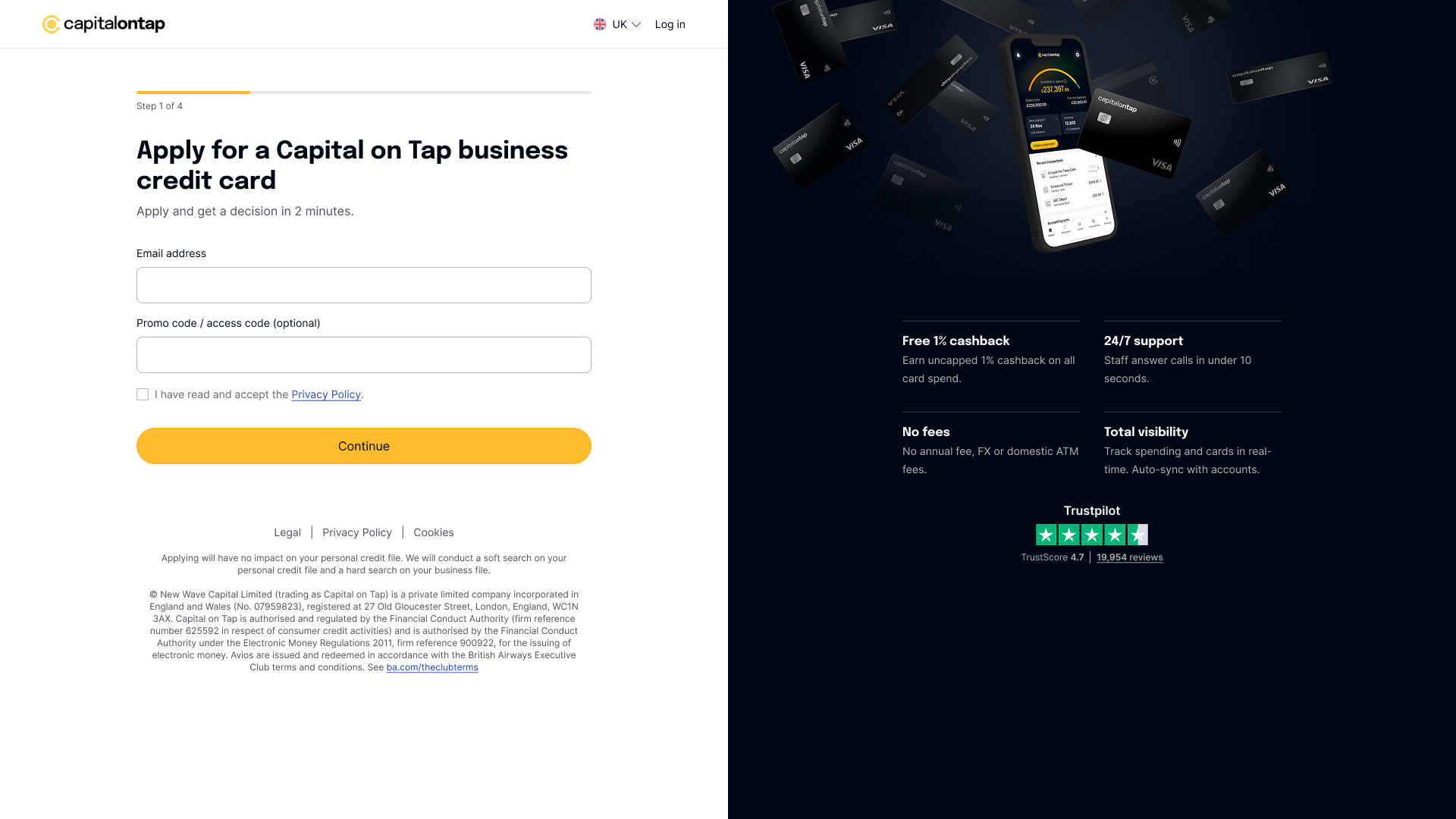

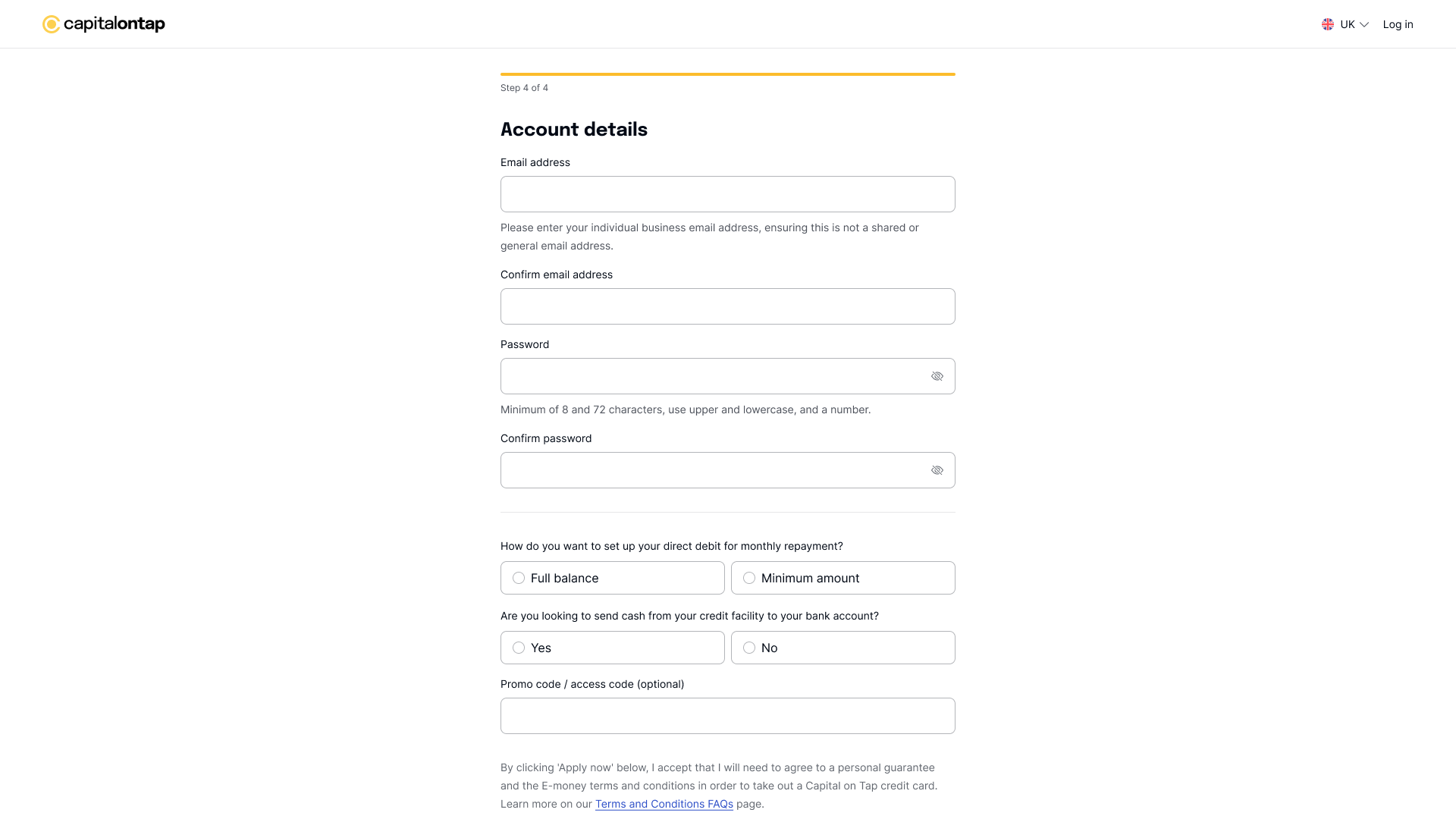

Who can apply: you qualify if you run a UK limited company, LLP or PLC active at Companies House with no unsatisfied CCJs in the last 12 months. Sole traders and partnerships can’t apply, and you don’t need to move your banking to qualify.

What you need to apply: your company registration number and director details, not bank statements or trading history. If your accountant files your confirmation statement and self-assessment, your details are already in order.

Approval timing: decisions can land within hours, and you get an instant virtual card on approval while the physical card ships separately.

Credit checks: applying is a soft search with no credit-file impact until you accept an offer; accepting triggers a hard search. Use it to see your real offered rate before you commit.

Personal guarantee: approval needs a personal guarantee from a director or major shareholder, so if the business can’t clear the debt, you’re personally liable. Confirm your offered rate before you draw down.

Fees, APR and Repayments

| Fees and rates | Detail |

|---|---|

| Rates from | 13.86% (floor rate) |

| Representative APR | 34.9% |

| Average rate (Q4 2025) | 46.05% |

| Interest-free period | Up to 42 days if cleared in full |

| Annual fee | £0 (free card) |

| Pro card fee | £299/year |

| Foreign transaction fee | None |

| ATM withdrawal fee | None (interest still applies) |

| Cashback | 1% uncapped (free); 0.5% (Pro) |

| Example borrowing cost | £10,000 for one month at 46% costs ~£383 in interest |

| Verified 23 July 2026. | |

Representative APR and Offered Rates

If you carry a balance, plan for 46% APR, not 13.86%. The 13.86% is the floor; the FCA representative rate is 34.9%. Capital on Tap discloses its actual Q4 2025 average: 46.05%.

If you carry a balance, S&P Global Ratings data (London Cards No. 1 and No. 2 securitisations) shows the rate band runs BBR+9.9% to BBR+49.9%, with ~35% portfolio yield. The 46.05% average sits in the upper half.

The floor rate is marketing; your offered rate is the catch. That gap is what costs you.

Interest-Free Period

Capital on Tap gives you up to 42 days interest-free on card spending, but only if you pay your statement balance in full and on time each month. Clear it in full and your purchases cost nothing in interest.

Carry any balance past the due date and interest applies at your offered rate, which averaged 46.05% in Q4 2025. We read this as a reward for discipline, not cheap credit.

If your cash flow is lumpy, treat the 42 days as breathing room between paying a supplier and being paid, not as a loan. Used that way it costs nothing; used as borrowing, it quietly becomes the most expensive part of the card.

When Interest Outweighs Rewards

Calculate the cost: a £10,000 balance for one month at 46% APR costs £383 in interest. At the floor rate, it costs £115, a £268 gap.

If you’re an e-commerce company carrying £10,000 during stock purchasing, at 40% APR one month costs £333 interest. Annual cashback at £5,000/month spend is £600. Three carried months wipe out two-thirds of cashback.

Industry data shows 84% of micro-businesses and 94% of small businesses clear monthly; in construction, only 35% do. If yours carries balances, the rate is the first decision point.

If your offered rate comes back above 25% and you carry a balance, a card with a fixed representative rate you can confirm upfront will cost you less than an uncertain offer here.

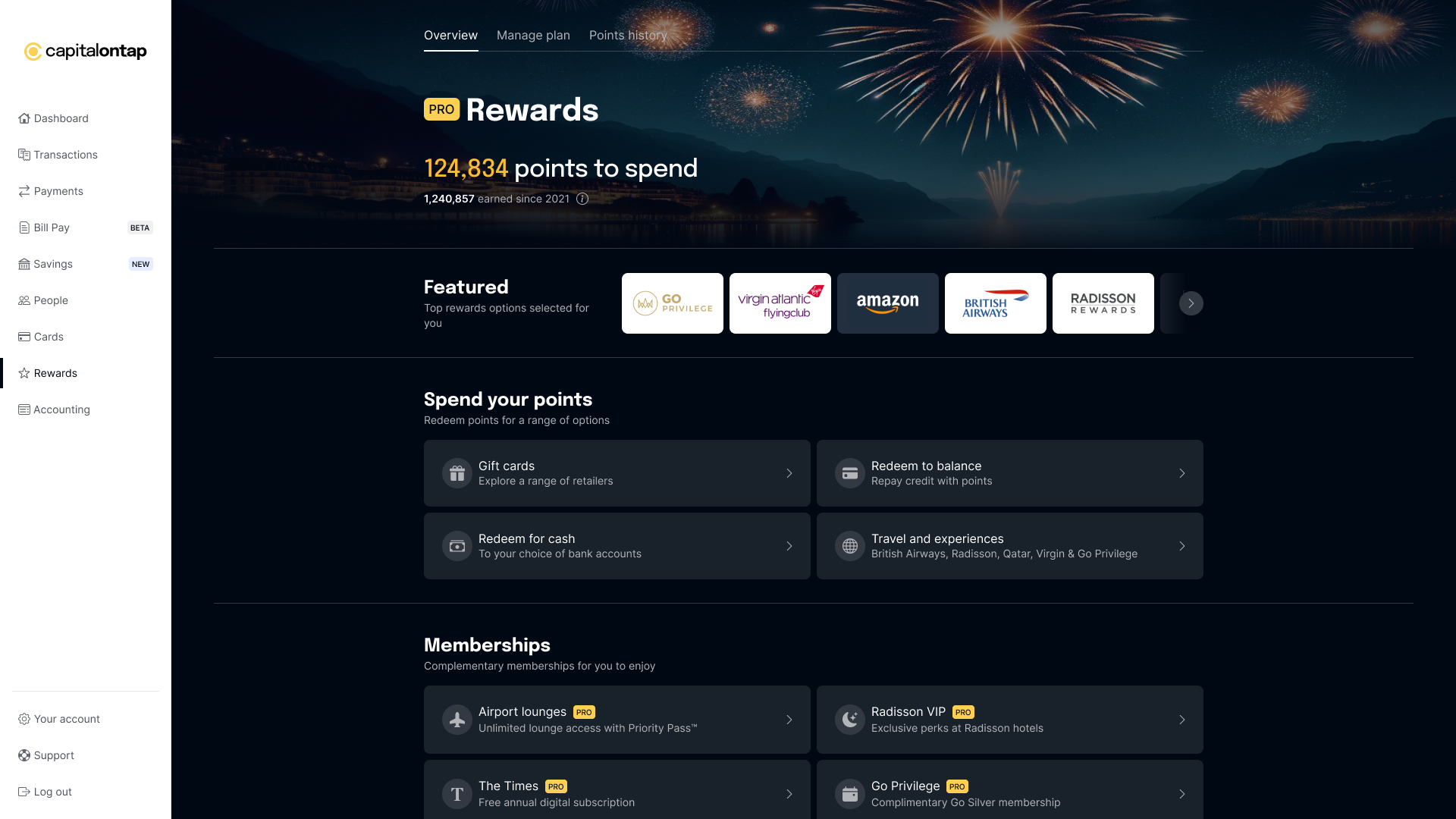

Rewards, Cashback and Avios

Free Card Rewards

At the free tier you earn 1% cashback on all spend, uncapped and with no annual fee. Take it as statement credit or gift cards, or convert points to Avios or Virgin Points.

If you take air miles instead of cashback, the free card converts 10 points to 8 Avios through the British Airways or Qatar Airways clubs. For most businesses that clear monthly, we rate the free card as the right default.

Pro Card Rewards

Pro costs £299/year and changes the maths: cashback drops to 0.5%, but Avios conversion improves to 1 point per Avios. Pro also adds 10,000 bonus points when you spend £5,000 in your first three months.

You earn the £299 back only above roughly £60,000 annual spend, or if you fly often enough to use the better Avios rate. Below that, the free card wins.

We confirmed Pro’s fee and the 0.5% cashback rate from Capital on Tap’s published product pages in March 2026.

Free vs Pro

| Feature | Free Card | Pro Card |

|---|---|---|

| Annual fee | £0 | £299/year |

| Cashback | 1% uncapped | 0.5% |

| Avios conversion | 10 points = 8 Avios | 1 point = 1 Avios |

| Virgin Points | Yes | Yes |

| Sign-up bonus | None | 10,000 points for £5,000 spend in 3 months |

| Best for | Spend under £60k/year | High spenders and frequent flyers |

| Verified 23 July 2026. | ||

If you spend under £60,000 annually, stick with free: 1% cashback is better than Pro’s 0.5% minus £299 fee. We ran the break-even calculation across several spending levels to confirm this threshold.

Your marketing director runs £4,000/month in ad spend and SaaS tools. Free tier earns £480/year. Pro on the same spend earns £240 minus £299, a net loss.

Your Pro fee is £299/year and cashback drops to 0.5%, confirmed from Capital on Tap’s published product pages in March 2026.

Features and Spending Controls

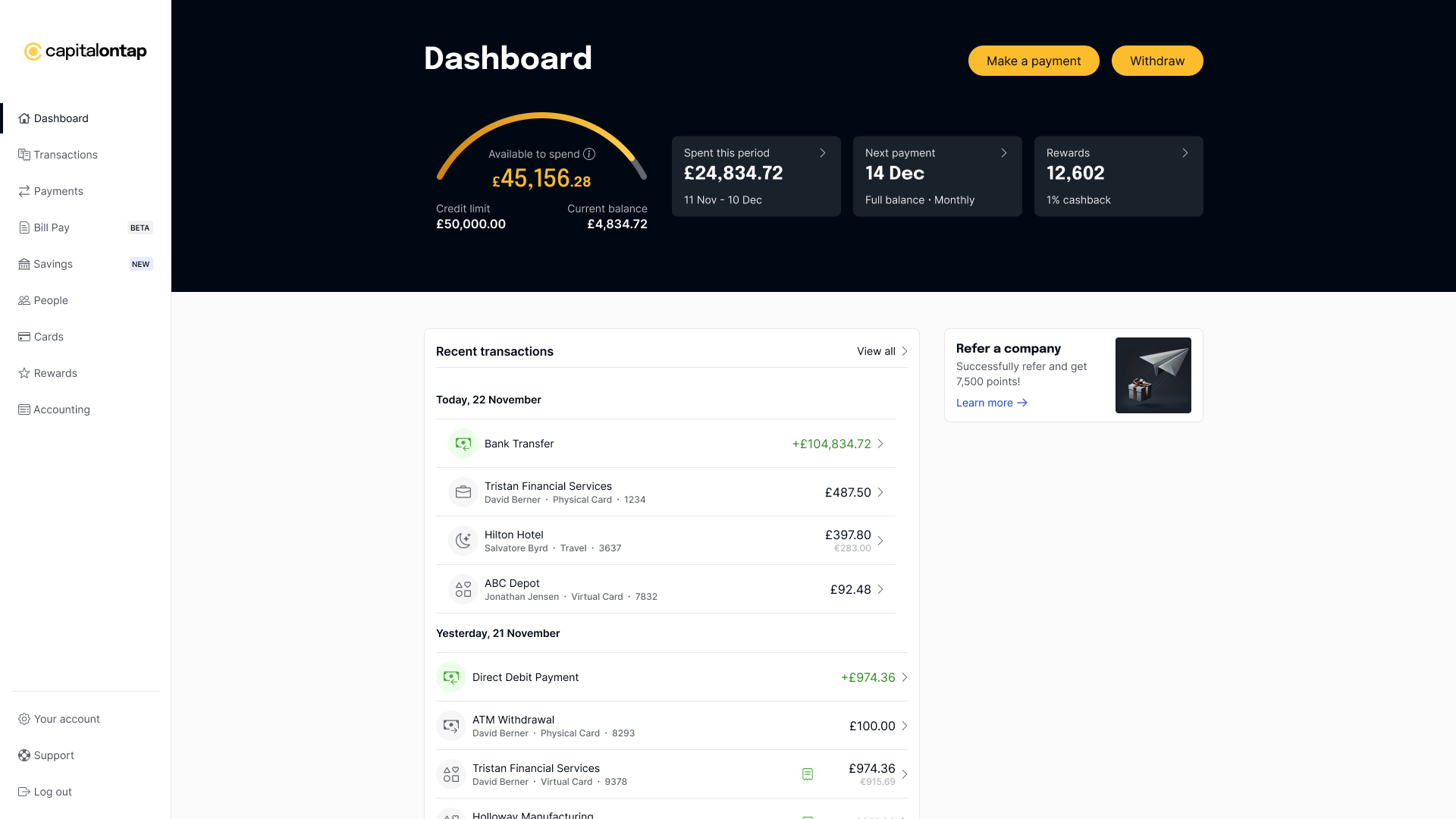

Employee cards: you can issue cards to staff at no extra cost, set per-card limits, and track spend in one place. When your sales team is back from a Tuesday client dinner and you need expenses reconciled by Friday, that removes the receipt-chasing.

Expense controls: you get receipt capture and smart categorisation, so a stationery purchase lands as Office Supplies, but the controls are basic. If you need approval workflows before each purchase clears, Moss is a closer fit.

Accounting integrations: if you run your books in Sage, Xero, QuickBooks or FreeAgent, Capital on Tap links to all four directly, syncing transactions daily and auto-categorising by merchant. File quarterly VAT and your return builds from reconciled data, not a month-end scramble.

You can pull in up to 90 days of past data when you first connect; if you use none of the four, transactions still export to CSV.

Overseas Spending

If you pay overseas suppliers or travel for client meetings, Capital on Tap charges no foreign transaction fees and no ATM withdrawal fees. We verified this from its published fee schedule in March 2026, making it one of the cheaper international options.

Overseas card spend, paying overseas suppliers, and travel: the Visa network is widely accepted and there’s no FX surcharge on purchases.

Purchases convert at the Visa exchange rate. Cash withdrawals are fee-free but still accrue interest from day one, and business cards carry weaker dispute protection than personal cards.

Regulation, Protection and Personal Guarantee

| Protection | Where you stand |

|---|---|

| FCA status | Authorised and regulated (firm reference 625592) |

| Is it a bank? | No, a lender (New Wave Capital Limited) |

| FSCS protection | Not applicable (no deposits held) |

| Personal guarantee | Required from a director or major shareholder |

| Director liability | You are personally liable if the business defaults |

| Section 75 | Not available on business cards |

| Visa chargeback | Available, but a weaker alternative |

| Missed payments | Interest at your offered rate; can affect your credit file |

| Verified 23 July 2026. | |

Is it regulated: yes, and it shapes your risk. Capital on Tap (New Wave Capital Limited, FRN 625592, Companies House 07959823) is FCA-authorised but a lender, not a bank. Your money isn’t FSCS-protected, though that doesn’t affect you when borrowing rather than depositing.

Personal guarantee: you sign one as a director or major shareholder, so if the business can’t clear the debt, you’re personally liable. The limit sits with the company; the risk sits with you. Confirm your offered rate before you draw down.

Chargeback and Section 75: you don’t get Section 75 on a business card. If a supplier fails to deliver, you’re limited to Visa chargeback, a weaker route. Weigh that before a large deposit to a new supplier.

Customer Reviews

You’ll see a high headline on Trustpilot, 4.7 out of 5 across more than 18,000 reviews, but the split underneath should shape your expectations more than the score. Positive reviews cite fast approval and high credit limits. We last checked the profile in June 2026.

You’ll see negative reviews cluster around rate surprises: customers offered rates far above the 13.86% advertised floor, aligning with the 46.05% Q4 2025 average we documented.

In practice, the rate surprise is avoidable: when you apply it’s a soft search, so you can check your actual offered rate before committing and walk away free if it’s higher than you expected. The complaints come mostly from applicants who banked on the headline floor.

Alternatives to Capital on Tap

If Capital on Tap’s rate uncertainty or sole-trader exclusion rules it out for you, three alternatives are worth a look. We weighed each against the specific weakness it fixes: a predictable upfront rate, access for sole traders, or tighter spend controls.

Final Verdict: Is Capital on Tap Worth It?

Capital on Tap is strong if you clear the balance every month. You get limits up to £250,000, 1% uncapped cashback or Avios, and up to 42 days interest-free, all without switching your business bank account.

It turns risky the moment you carry a balance. The 13.86% floor isn’t what most people pay; the Q4 2025 average was 46.05%. Check your offered rate on the soft search before you draw down.

If you’re a sole trader or partnership, it’s a non-starter: Capital on Tap only accepts limited companies, LLPs and PLCs. A high-street business card or a provider that accepts sole traders is your realistic route instead.

Clear it in full each month and you stay ahead; let a balance run and the 46% does the damage.

Frequently Asked Questions

What APR will I actually get with Capital on Tap?

The starting rate is from 13.86%, the representative APR is 34.9%, and the average rate paid by new customers in Q4 2025 was 46.05%. Your individual rate depends on your company’s credit profile and is only confirmed after you apply. The application is a soft search, so checking your rate doesn’t affect your credit file.

Can sole traders get a Capital on Tap card?

No. Capital on Tap is restricted to UK limited companies, LLPs and PLCs registered at Companies House. Sole traders and partnerships can’t apply, so you would need a card that accepts sole traders directly, such as a high-street business account card.

Does Capital on Tap have an interest-free period?

Yes. You get up to 42 days interest-free on card purchases, but only if you pay your statement balance in full and on time each month. Carry a balance past the due date and interest applies at your offered rate, which averaged 46.05% in Q4 2025.

Is Capital on Tap a real bank, and is it legit?

It’s legitimate, but it isn’t a bank. Capital on Tap is the trading name of New Wave Capital Limited, authorised and regulated by the FCA (firm reference 625592) and registered at Companies House (07959823); it has lent to UK businesses for over a decade and issues cards on the Visa network. As a fintech lender rather than a bank it carries no FSCS deposit protection, but since you’re borrowing rather than depositing, that distinction isn’t relevant here.

How much cashback does Capital on Tap pay?

The free tier pays 1% cashback on all spend. The Pro tier (£299/year) pays 0.5% cashback. You need roughly £60,000 in annual spend for the Pro tier cashback to offset the annual fee.

Is Capital on Tap Pro worth it?

Pro costs £299/year, pays 0.5% cashback (versus 1% on the free card) and improves Avios conversion to 1 point per Avios, plus 10,000 bonus points for £5,000 spent in three months. It mainly pays off above roughly £60,000 annual spend, or for directors who fly regularly. Below that, the free card wins.

Does Capital on Tap charge foreign transaction fees?

No. Capital on Tap doesn’t charge foreign transaction fees or ATM withdrawal fees, making it one of the cheaper options for overseas business spending. Cash withdrawals are fee-free but still accrue interest from the day you take them out.

How fast can I get a Capital on Tap card?

Decisions can come within hours. On approval, you receive an instant virtual card you can use immediately while waiting for the physical card to arrive.

What credit limit can I get with Capital on Tap?

Limits run up to £250,000, which is significantly higher than most bank-issued business cards. Your actual limit depends on your company’s financials and credit profile.

Does Capital on Tap require a personal guarantee?

Yes. Capital on Tap requires a personal guarantee from a company director or major shareholder when you apply. That means if the business can’t clear the card debt, you’re personally responsible for repaying it. The credit limit sits with the company, but the ultimate liability sits with you, which is one more reason to be sure of the rate you’re actually offered before you draw down.

Can you earn Avios with Capital on Tap?

Yes. Instead of taking your points as cashback, you can convert them to Avios through the British Airways Club or Qatar Airways Privilege Club. On the free card the rate is 10 points to 8 Avios; on the Pro card (£299/year) it improves to 1 point per Avios, and Pro adds 10,000 bonus points when you spend £5,000 in your first three months. Points also convert to Virgin Points or gift cards. For a director who flies regularly, Pro’s better conversion is where the annual fee can start to pay for itself.

Methodology and Disclosure

How we reviewed Capital on Tap Credit Card

What we assessed. We evaluated Capital on Tap Credit Card on pricing, contract terms, features, and eligibility. These are the factors that matter most to UK small businesses considering this provider.

Data sources. Capital on Tap Credit Card’s pricing page, terms, and product docs were checked directly in April 2026. No comparison sites, no press releases, no affiliate material. FCA register cross-checked for regulatory status.

Update cadence. We re-verify this page at least monthly, and whenever a provider changes pricing, eligibility, or terms. The verification date on the page reflects the most recent full review. Some links on this page are affiliate links, see our editorial policy.