Square is a major global payment processing platform that allows businesses to accept payments in person, online, and over the phone. They process over $100bn annually.

Square is one of the best ways to start taking payments for your business because they’re:

- Simple – All of their card machines are easy to set up and operate, even with no prior experience.

- Affordable – Square offers competitive transaction fees of 1.7% with no monthly fees or long-term contracts.

- Versatile – Get paid in-person, online, via an invoice or over the phone.

- Quick to Pay – Square offers fast next-day funding so you can get access to your earnings quickly.

- Secure – Strong encryption and fraud prevention tools protect your data and keep customers safe.

- 30-Day Trial – Try Square’s subscription services for free for 30 days.

Below, my detailed review examines Square’s features, pricing, and security in more detail to help you decide if it is the right way for your business to take payments.

You can also read our article here, which summarises the best card machines for business in 2024.

Square Review: My Verdict

Square is one of my top recommendations for retail and hospitality businesses that want a flexible, reliable, and easy-to-use payment system. You can accept payments in-store, online, or via invoice, giving you the freedom to operate across multiple sales channels with minimal fuss.

Its combination of intuitive software and sleek hardware makes managing sales, inventory, and customer data feel effortless. Everything lives in one streamlined system that’s designed to scale with your business.

The pricing is simple. With a pay-as-you-go model and no monthly fees, Square is ideal for smaller businesses that want clarity and control over costs.

Security is excellent. Square is PCI-DSS compliant and includes advanced encryption and fraud prevention. That said, some businesses have reported sudden account suspensions, so it’s worth being aware of the risk.

Customer support is solid overall. The self-service tools are well designed and helpful, and while response times were mostly fast, I did experience a couple of slower moments during testing.

In short, Square offers powerful tools with minimal complexity. If you’re looking for a transparent, modern payment solution that just works, it’s a very strong contender.

Pros and Cons of Square

Square: Overview

Square gives you a lot of ways to take payments, not just in person but also online and over the phone.

First, let’s talk about taking payments on your website. Square provides a straightforward way to integrate its payment system into your online store. Its standalone website offering is somewhat basic, though, so you’re better off integrating it with your existing site rather than using their own e-commerce platform. If you’re a Shopify user, it’s as easy as adding the Square APP, or, in WordPress, you can download the plugin for one-click installation.

Invoicing with Square is also simple. You can send invoices right from the app or your computer, and they look professional. But be aware that if you send a lot of invoices, the fees can add up. The invoice itself can be generated and sent for free, but once the customer pays the invoice online via credit or debit card, Square’s standard processing fee for online transactions is applied.

Taking payments over the phone is also straightforward with Square. You just key in the customer’s card details into the system, and you’re good to go. It’s handy, but remember, the fees for this are higher than if the customer swipes their card in person.

Lastly, if you’re tech-savvy, you can use Square’s API to get it working just the way you want with your own app or website.

Square Features

The following section delineates the features and services offered by Square Payments.

| Feature | Availability | Notes |

|---|---|---|

| Card Payment Acceptance | ✓ | Accepts Visa, Mastercard, American Express, etc. |

| Contactless Payment Options | ✓ | Supports NFC payments including Apple Pay, Google Pay |

| Quick Payment Processing | ✓ | Option for same-day payments |

| Inventory Management | ✓ | Real-time tracking and low-stock alerts |

| Data Analytics Dashboard | ✓ | User-friendly interface for sales insights |

| Gift Cards & Loyalty Programs | ✓ | Fully customisable |

| Phone Payments | ✓ | Manual card information entry |

| API and Software Integration | ✓ | Free APIs and SDKs for custom integrations |

| Variety of Card Readers | ✓ | Different models available at multiple price points |

| Seamless POS Integration | ✓ | Square POS app compatible with various hardware options |

| Online Payment Solutions | ✓ | Free online store setup, social media sales channels |

| Remote Payment Options | ✓ | Digital invoices and checkout links available |

Square Appointments

Square Appointments is a cloud-based tool made for businesses to manage bookings, customers, and staff. It’s easy to use and helps businesses organise their work and make more money.

Key Features:

- Online Booking: Lets customers book appointments online at any time.

- Reminders: Sends email and text reminders to customers so they don’t forget appointments.

- Recurring Appointments: Allows setting up regular appointments for customers.

- Manage Multiple Locations: Handle appointments for more than one place from one dashboard.

- Staff Management: Make staff profiles and set their work hours and services.

- Take Payments: Use Square to take payments both online and in person.

- Reports: Make reports to understand how your business is doing.

Square for Retail

Square for Retail is a tool for shops to manage products, sales, and customers. It’s designed to make retail work easier and help businesses make more money.

Key Features:

- Manage Products: Add and update product info, pricing, and how much you have in stock.

- Take Payments: Use Square’s tools to take credit cards, debit cards, and other payments.

- Keep Track of Stock: Know what’s in stock and get alerts when it’s time to reorder.

- Customer Info: Store information about customers and their buying habits.

- Reports: Create reports to see how well your shop is doing.

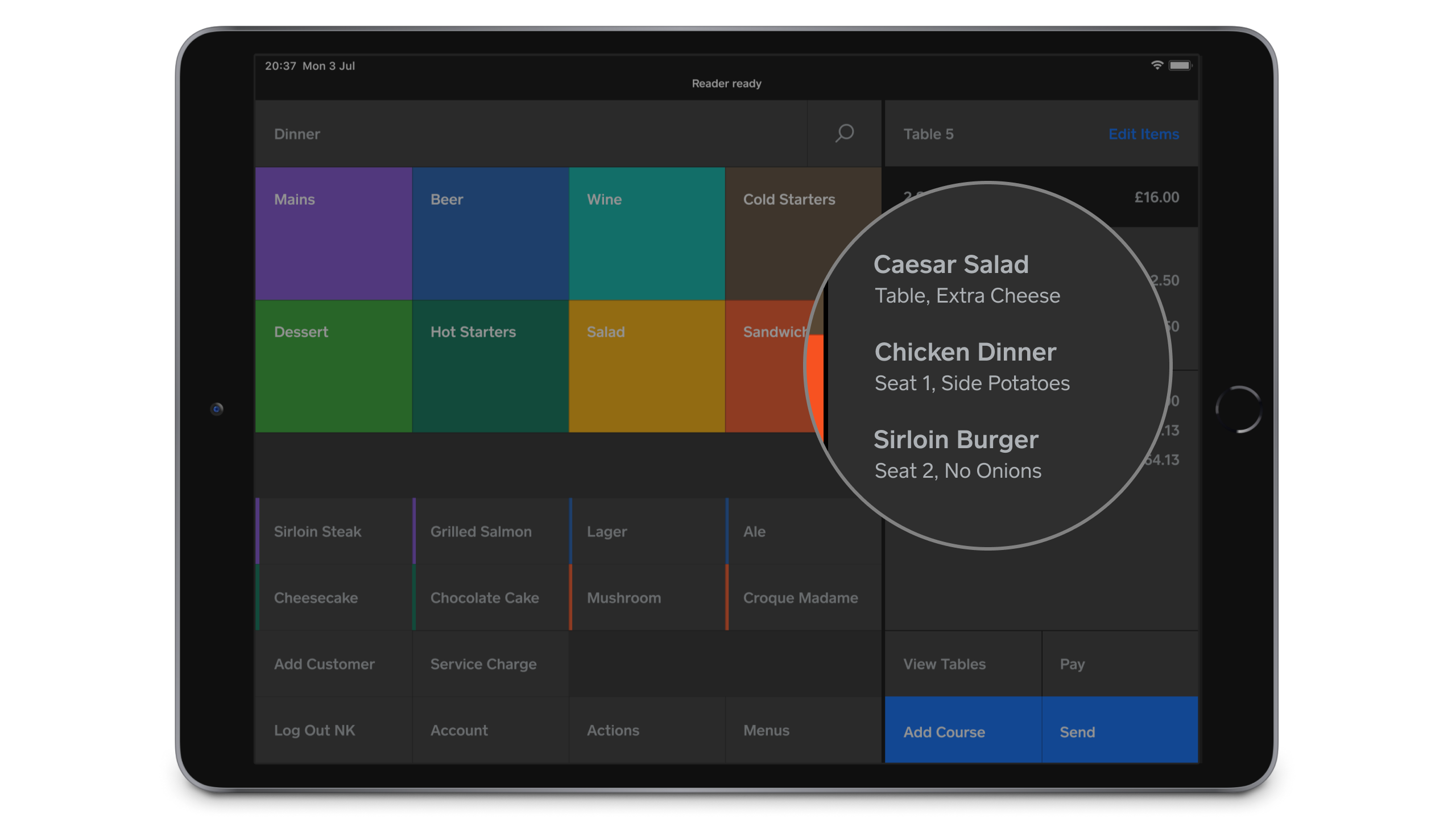

Square for Restaurants

Square for Restaurants is designed specifically for restaurant use. Its features help organise the restaurant and give customers a better experience.

Key Features:

- Table Management: Keep track of tables and reservations.

- Manage Menus: Add and update food and drink items easily.

- Kitchen Display: Send orders to the kitchen and see their status.

- Staff Management: Make staff profiles and set their roles.

- Take Payments: Use Square to handle payments in different ways.

- Reports: Create reports to understand how the restaurant is doing

Square POS System Review

On the positive side, Square is incredibly easy to set up and intuitive to use on a daily basis. The interface is clean and simple enough for even non-tech-savvy staff to learn with minimal training. Square also makes the payment process seamless—their mobile card readers are convenient and portable and integrate well across online and offline sales channels.

The basic POS features Square offers for free cover most retail business needs, such as inventory management, discount application, email receipts, etc. The pay-as-you-go pricing model is beneficial for lean startups, as you only pay processing fees rather than monthly subscription costs.

Even more advanced users will find Square POS a comprehensive business tool. The internal reporting and analytics capabilities can grow with demand and are just as customisable as other higher-end systems. While Square integrates with many third-party platforms, some users may miss having native advanced features like warehouse management functions.

Also, while customer service is generally responsive, I wish they had more POS-specific support and onboarding guidance beyond the DIY approach and a couple of articles in their backend. Some users have also complained about sudden account suspensions and Square’s holding of funds without sufficient explanation.

Square Software Features

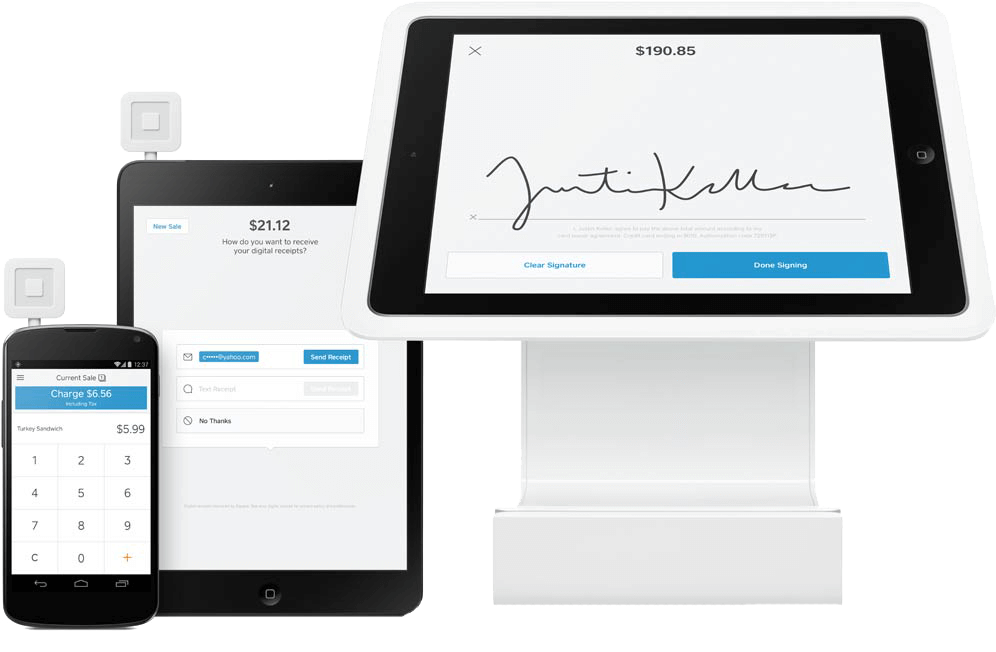

Square Hardware Options

Square provides a range of hardware solutions tailored to meet your specific needs:

- Square Reader: Priced at £19+VAT, it accepts chip, PIN, and contactless payments, featuring wireless connectivity.

- Square Terminal: At £149+VAT, this all-in-one wireless device accepts payments and prints receipts.

- Square Stand: Priced at £99+VAT, it converts an iPad into a full-fledged POS system by adding a card reader.

- Square Register: At £599+VAT, this Android-based POS comes with integrated payments, a barcode scanner, and a customer-facing display.

- Additional Hardware: Optional cash drawers, receipt printers, and barcode scanners are also available for added convenience.

Get 25% off Square Reader or Terminal with code SEP2025 until 25/10/2025*.

*Offer commences 04/09/2025 at 5pm and expires 25/10/2025 at 5:00pm UK time or while supplies last, whichever comes first. Offer is for 25% off total cost of Square Terminal and Reader excluding VAT. Limited to 3 devices per person. Each code is limited to one redemption per account holder. Valid for Square customers located in the UK only. Offer not valid with guest checkout. Square reserves the right to modify, revoke or cancel the offer at any time. Offer cannot be combined with any other coupon. Void where prohibited, not redeemable for cash, and non-transferable.

Square Software Pricing

The software itself is free, with transaction fees as follows:

- 1.75% for in-person payments using chip, PIN, or contactless methods.

- 2.5% for online payments and invoices.

There are no monthly fees or long-term contracts. Custom pricing is available for high-volume merchants processing over £200k annually.

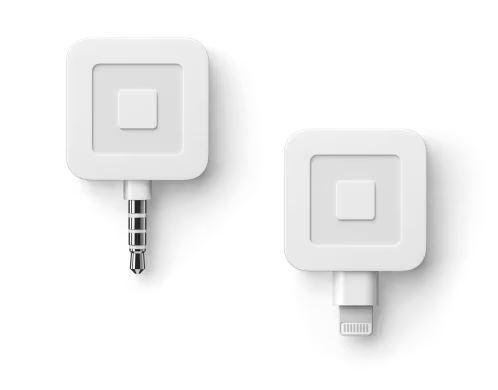

Should I Use the Square Card Reader? My Review

For many businesses, the entry point to Square is their Card reader, a small, portable device that allows businesses to accept card and contactless payments through a mobile device.

So, how good is it?

After testing it, I sense that the Square card reader is a nifty tool with a lot to recommend. One of the best parts is how simple it is to start using it. You just plug it into your phone or tablet, and you can start taking card payments right away. The reader itself only costs £19, which is a pretty low one-time cost.

It’s also quick to deposit money into your bank account, usually in 1-2 days. This can be really helpful for businesses that need fast access to their cash. Plus, it works really well with Square’s free software for taking payments and tracking sales, making it a good all-around tool for your business.

However, it’s not all good news. The fee for each sale you make is 1.75%, which might be higher than other options out there, like Revolut at 0.7%. Also, customers must enter their PIN on your device screen because there’s no separate keypad. This might not be ideal for some people.

If your business is in an industry that gets a lot of chargebacks, or if Square thinks there’s a high risk of fraud, you might find that they hold onto your money for more extended periods.

So, is the Square card reader worth it? Depending on your situation, yes, it’s one of the most affordable options out there with some of the most advanced features on offer. For businesses great and small, you can find scalable solutions to fit your needs.

How Secure is Square?

Square Payments takes security very seriously and uses a variety of measures to protect businesses and their customers, as follows:

- End-to-end encryption: All transactions are encrypted from the point of sale to Square’s servers using industry-standard encryption methods, which helps protect sensitive data from being intercepted.

- PCI compliance: Square is fully compliant with the Payment Card Industry Data Security Standard (PCI DSS), which is a set of security requirements designed to protect credit card data. This means that Square has taken the necessary steps to protect customer data.

- Two-factor authentication: Square offers two-factor authentication, which adds an extra layer of security to your account. With two-factor authentication, you will need to enter a code from your phone in addition to your password when logging in.

- Fraud monitoring: Square uses advanced fraud monitoring tools to detect and prevent fraudulent transactions. These tools help to protect businesses from financial losses.

- Employee access controls: Square allows businesses to control who has access to sensitive data. This helps to prevent unauthorised access to customer data.

- Customer information protection: Square stores customer data in a secure environment. This data is encrypted and protected from unauthorised access.

Square Pricing & Costs

Square Payments has a transparent and straightforward fee structure. There are no hidden fees or monthly charges.

| Transaction Type | Fee |

|---|---|

| Contactless, Chip and PIN, Swiped | 1.75% |

| Manually Keyed-In, Recurring, Invoices | 2.5% |

| UK Cards (Online Payment Products) | 1.4% + 25p |

| Non-UK Cards (Online Payment Products) | 2.5% + 25p |

| Account Activation | No Fee |

| Early Termination | No Fee |

| Interchange Fees | No Fee |

| Chargeback Fees | No Fee |

| Cash Payments | No Fee |

| Account Inactivity | No Fee |

| PCI Compliance | No Fee |

Fee invoicing and monitoring: Square allows you to view your current processing rates and fees anytime from your online Square Dashboard. Fees are deducted before each transfer and are not billed on a monthly basis.

Here are some additional things to consider when evaluating Square Payments fees:

- Volume discounts: Square offers volume discounts for businesses that process a high volume of transactions.

- Surcharges: Square allows businesses to add a surcharge to their prices to cover the cost of processing fees.

- International fees: Square charges additional fees for processing transactions in certain countries.

Square Payments Setup Guide

If you’re looking to integrate Square Payments into your business operations, understanding the setup process is essential for a smooth transition. This guide aims to walk you through each critical step.

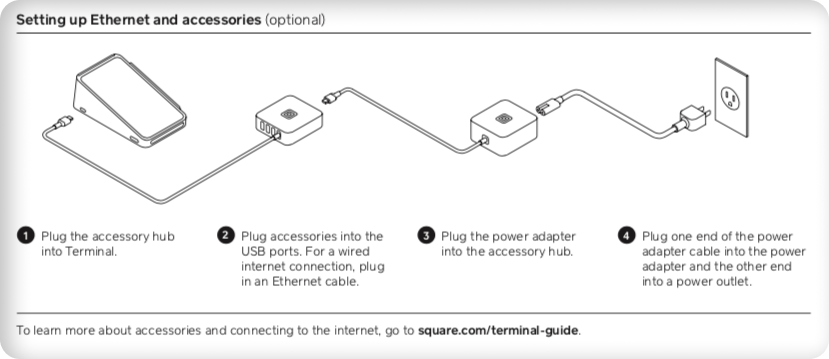

Hardware Setup

- Choose Your Hardware: Depending on your needs, select from Square’s range of card readers, terminals, or complete POS systems.

- Install the Hardware: Most Square hardware options are plug-and-play. Simply connect the device to a power source and your network.

Software Configuration

- Download the Square Point of Sale App: Available for both iOS and Android devices, the Square POS app is where you’ll manage most of your day-to-day operations.

- Configure Settings: Open the app and go through the initial setup process. You’ll be prompted to enter business details, set preferences, and possibly run a test transaction.

Online Integration

- Select an eCommerce Platform: If your business operates online, you’ll want to integrate Square with your online storefront. Square is compatible with many popular e-commerce platforms such as Shopify and WooCommerce.

- Follow the Platform-Specific Instructions: Once you’ve chosen an e-commerce platform, follow the specific installation guidelines for integrating Square as your payment processor.

Employee Training

- Familiarise Staff with Interface: The Square POS app is generally intuitive, but ensuring that all employees are comfortable with its functionalities is crucial.

- Set Employee Permissions: Square allows you to define roles and permissions for different staff members, enabling better control and security.

What’s the Customer Service like at Square?

Customer service quality is a big factor when choosing a payment processing system, as timely and effective support can dramatically influence your day-to-day operations. Square Payments offers multiple channels as follows:

- Online Help Centre: A well-stocked repository of articles and FAQs, ideal for solving common issues without requiring human intervention.

- Live Chat Support: Available during business hours, the live chat feature is useful for quick queries and minor issues.

- Phone Support: Provides a more personal touch and is better suited for resolving complex issues or emergencies.

- Email Support: Suitable for non-urgent queries, with response times usually within 24 hours.

While Square Payments offers a range of customer support options, it’s important to note that some business owners have reported varying levels of satisfaction with the service. Be sure to check if the type of support you require—be it 24/7 phone service or extensive self-help resources—is adequately provided by Square.

Square Payments Reporting and Analytics

Data-driven insights are indispensable for any business aiming to refine its operations and improve profitability. Square Payments provides robust reporting and analytics tools designed to furnish you with valuable data.

- Sales Summary: A detailed breakdown of sales activity, segmented by time period, location, or even specific items.

- Inventory Reports: Keep track of stock levels and identify trends to make informed purchasing decisions.

- Employee Performance: Evaluate staff productivity by tracking sales against hours worked.

- Customer Engagement: Monitor customer behaviour, including frequency of visits and average spend, to tailor marketing strategies effectively.

- Payment Methods: Analyse the popularity of different payment methods among your customers, which can guide your future infrastructure investments.

Square’s reporting and analytics suite is generally considered comprehensive and user-friendly. However, it may not offer the depth of analysis that some businesses with more complex data analytics needs might require. For those cases, integration with external analytics tools may be necessary.

Square Payments Integrations

Square Payments has made sure its platform is compatible with a variety of third-party applications. Here’s a selection:

- Accounting Software: QuickBooks, Xero, and other accounting platforms are easily integrated, facilitating streamlined financial management.

- Inventory Management: Connect with popular inventory systems like Shopventory or Stitch Labs to maintain accurate stock levels across platforms.

- eCommerce Platforms: Compatibility with leading online storefronts like Shopify, WooCommerce, and BigCommerce allows for an integrated omnichannel experience.

- Employee Management: Integrate with HR solutions for efficient staff scheduling, time tracking, and payroll management.

- Marketing Tools: Sync your customer data with marketing platforms like Mailchimp to run targeted campaigns effectively.

What Payments Methods does Square support?

Square Payments offers a variety of payment methods to accommodate the needs of businesses of all sizes.

- Card payments: Square Payments accepts all major credit and debit cards, including Visa, Mastercard, American Express, Discover, and JCB.

- Contactless payments: Square Payments supports contactless payments using Apple Pay, Google Pay, and other NFC-enabled payment methods.

- Manual entry: Square Payments allows businesses to manually enter credit card information for payments over the phone or when the physical card is not present.

- Invoicing: Square Payments allows businesses to send digital invoices to customers, which they can pay online.

- Online checkout links: Square Payments allows businesses to create clickable links that customers can use to make payments online.

- ACH payments: Square Payments offers ACH payments for businesses that need to accept payments from bank accounts.

- Direct bank transfers: Square Payments offers direct bank transfers for businesses that need to accept payments from bank accounts.

Square Payments Card Readers and Hardware

Selecting the right hardware is pivotal for a seamless point-of-sale experience. Square Payments provides a range of hardware options designed to cater to various business needs:

- Square Reader: A pocket-sized card reader that pairs with mobile devices for a portable payment solution.

- Square Terminal: A standalone device that combines card reading and receipt printing functionalities, ideal for retailers or service providers.

- Square Register: A fully integrated point-of-sale system with a customer-facing display, tailored for more extensive retail setups.

- Additional Accessories: Cash drawers, receipt printers, and barcode scanners can be purchased separately and integrated easily with Square’s main hardware units.

Square Payments’ hardware options are generally lauded for their ease of use and stylish design. However, businesses with more complex point-of-sale requirements may need to consider additional hardware solutions that can integrate with Square’s system.

Square Payments Invoicing

Square Payments provides a comprehensive invoicing system with the following key features:

- Custom Invoices: Ability to create branded, detailed invoices directly within the Square app.

- Automated Reminders: Sends automated follow-ups to customers for unpaid invoices, reducing the manual workload.

- Invoice Tracking: Allows you to monitor the status of sent invoices, including when they are viewed and paid.

- Payment Scheduling: Provides options for customers to make partial payments or set up a payment schedule.

- Instant Payments: As soon as the invoice is paid, the funds are available in your Square account.

Square Reviews

Overall the Trustpilot reviews for Square seem largely positive, with a 4.1 star score of ‘great’ over more than 2100 reviews.

Most negative critiques relate to specific pain points, like customer support wait times. Many customers highlight the easy setup and transparent fees as big pros.

Positive Reviews:

- 80% of the reviews are five stars. Many customers mention easy setup, fast payments, and great customer service.

- Customers like the versatility for seasonal businesses or occasional payments. There are no monthly fees; you only pay per transaction.

- Appreciate the fast next-day funding and instant deposit options.

- Positive mentions of the hardware, like readers and point of sale, being easy to use.

Negative Reviews:

- 12% are 1-star reviews. The main complaints are around customer support issues like long wait times.

- Some experiences of accounts being suddenly suspended without explanation.

- Frustration with hardware failures and the warranty/replacement process.

- A few complaints about high card fees, though some got them lowered.

- Some limitations are mentioned, such as the fact that there’s no ability to accept deposits or pre-authorise cards.

- A couple of the reviews cited issues with integrated services like Weebly website builder after Square’s acquisition.

FAQs

How can I integrate Square with my other business software?

Square integrates with a wide variety of third-party software, including accounting software, CRM software, and e-commerce platforms. This makes it easy to streamline your business operations and get the most out of Square.

What are the benefits of using Square for international payments?

Square offers competitive exchange rates and low fees for international payments. You can also accept payments from customers in over 135 currencies, and Square will automatically convert the funds to your local currency.

How can I use Square to manage my employees?

Square offers a variety of employee management features, such as time tracking, payroll, and benefits. This can help you save time and money, and make it easier to manage your workforce.

How can I get support for Square?

Square offers a variety of support options, including 24/7 phone and email support, live chat support, and a comprehensive knowledge base. You can also get support from the Square community forum.

What are the different types of Square hardware?

Square offers a variety of hardware options, including:

* Square Reader: A small, portable card reader that can be plugged into your smartphone or tablet.

* Square Terminal: A countertop POS system that includes a touchscreen display, card reader, and receipt printer.

* Square Register: A full-fledged POS system that includes a touchscreen display, card reader, receipt printer, and cash drawer.

* Square Stand: A tablet stand that includes a card reader and receipt printer.

What are the different types of Square hardware?

Square offers a variety of hardware options, including:

* Square Reader: A small, portable card reader that can be plugged into your smartphone or tablet.

* Square Terminal: A countertop POS system that includes a touchscreen display, card reader, and receipt printer.

* Square Register: A full-fledged POS system that includes a touchscreen display, card reader, receipt printer, and cash drawer.

* Square Stand: A tablet stand that includes a card reader and receipt printer.